Scholastic (SCHL): Should You Buy, Sell, or Hold After Q4 Results?

Scholastic’s Recent Surge: What Should Investors Do?

Scholastic’s stock has experienced a remarkable climb, jumping 41% over the last half-year to reach $34.95 per share. This impressive rally may leave investors questioning the best course of action.

Is this a good opportunity to purchase Scholastic shares, or is it wise to proceed with caution before adding it to your investment portfolio?

Why We Believe Scholastic May Not Outperform

While it’s great to see investors benefit from recent gains, we remain skeptical about Scholastic’s prospects. Below, we outline three reasons why we see more attractive alternatives to SCHL, including a stock we prefer.

1. Weak Long-Term Revenue Growth

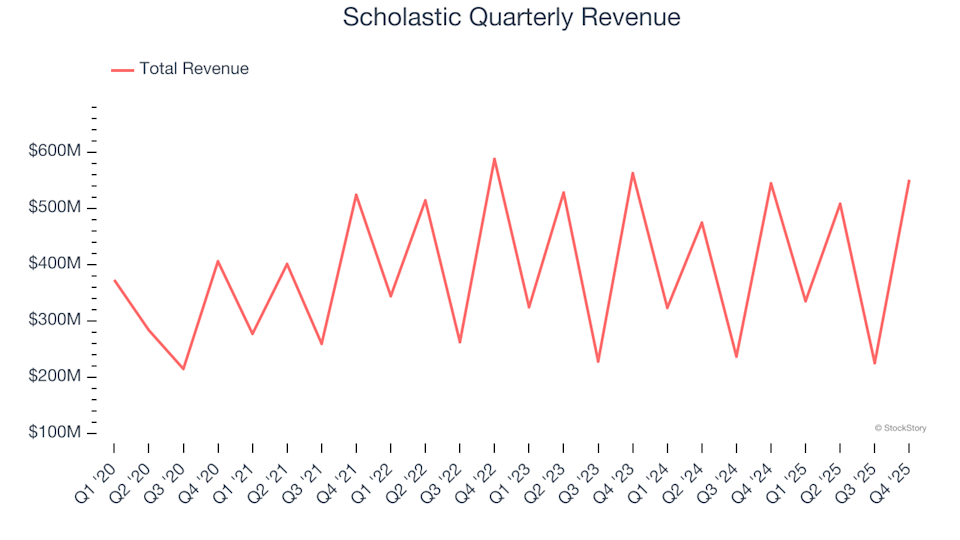

Consistent sales growth over the years is a hallmark of a strong business. While any company can enjoy short-term momentum, sustained expansion is a different story. Scholastic’s annualized revenue growth of just 4.9% over the past five years falls short of what we expect from leaders in the consumer discretionary sector.

Scholastic Quarterly Revenue

2. Limited Free Cash Flow Restricts Growth

At StockStory, we place a strong emphasis on free cash flow, as it’s the true measure of a company’s ability to pay its bills and reward shareholders. Over the past two years, Scholastic has barely broken even in terms of free cash flow, which limits its capacity to reinvest or return value to investors.

Scholastic Trailing 12-Month Free Cash Flow Margin

3. Declining ROIC Signals Fewer Profitable Opportunities

We favor companies that consistently deliver high returns on invested capital (ROIC), but it’s the direction of ROIC that often drives stock performance. Unfortunately, Scholastic’s ROIC has been on the decline in recent years. Combined with already modest returns, this trend suggests that the company’s opportunities for profitable growth are becoming increasingly scarce.

Scholastic Trailing 12-Month Return On Invested Capital

Our Verdict

Scholastic does not meet our standards for a high-quality investment. Despite its recent price jump, the stock is trading at a forward P/E of 24.1 (or $34.95 per share), which we consider reasonable, but we remain unconvinced about the company’s future. There are stronger options available in the market. For example, we recommend one of our favorite software stocks as a better alternative.

Top Stocks to Weather Any Market

Don’t Miss: This Week’s Top 6 Stock Picks. The current market is quickly distinguishing between true quality and overpriced names, with AI-driven shifts shaking up entire sectors. In such a fast-moving environment, you need more than just a list of good companies.

Our AI-powered system identified Palantir before its 1,662% surge, AppLovin ahead of its 753% rally, and Nvidia before its 1,178% climb. Every week, it highlights six new stocks that pass our rigorous criteria.

Our selections have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known gems such as Tecnoglass, which delivered a 1,754% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Seasoned Traders Eye Bitcoin and Ethereum Signals as Crypto Downturn Deepens

Decent Holding Stock Surges After FY25 Sales Boost

Why tokenization could make Solana a CLARITY Act winner

The unexpected Iran conflict did not discourage the dovish members of Poland's central bank