3 Reasons Why SentinelOne (S) Has Won Us Over

SentinelOne’s Recent Stock Performance

Over the past six months, SentinelOne has experienced a significant decline, with its share price falling by 27.2% since September 2025, now trading at $13.21. This downturn may have investors reconsidering their strategies.

With this drop in mind, is it the right moment to invest in SentinelOne? to learn more.

What Makes SentinelOne Stand Out?

SentinelOne (NYSE:S) is built on the concept of leveraging artificial intelligence to combat cyber threats. Its autonomous cybersecurity platform is designed to proactively prevent, identify, and address risks across endpoints, cloud environments, and identity infrastructures.

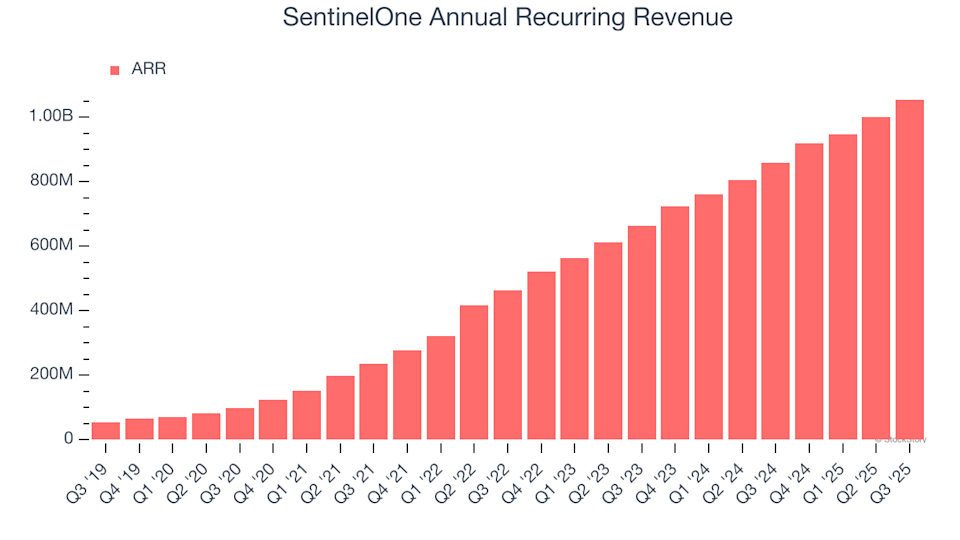

1. Impressive Growth in Recurring Revenue

Unlike total revenue, which can include lower-margin services, annual recurring revenue (ARR) focuses solely on contracted software subscriptions, providing a clearer picture of a SaaS company’s stable, high-margin income.

In the third quarter, SentinelOne reported ARR of $1.06 billion. Over the past year, its ARR has grown at an average annual rate of 24.6%. This robust expansion demonstrates strong customer confidence in the company’s technology and enhances the predictability of its business, a quality that often appeals to investors.

SentinelOne Annual Recurring Revenue

2. Strong Revenue Projections

Analyst forecasts can provide insight into a company’s future prospects. While projections are not always precise, accelerating revenue growth tends to support higher valuations, whereas slowing growth can have the opposite effect, though some slowdown is natural as companies mature.

Looking ahead, Wall Street expects SentinelOne’s revenue to climb by 20.1% over the next year. Although this is below the 29.1% annualized growth seen in the previous two years, it still signals confidence in the company’s offerings and continued market traction.

3. Anticipated Improvements in Free Cash Flow

Free cash flow is a key metric for evaluating a company’s financial health, as it reflects the cash available to cover expenses and fuel growth. Ultimately, cash flow is more important than accounting profits when it comes to meeting obligations.

Analysts anticipate that SentinelOne will see better cash conversion in the coming year. Consensus estimates suggest its free cash flow margin, which stood at 4.7% over the past year, could rise to 10%.

Our Takeaway

These factors highlight why SentinelOne is an appealing business. Following its recent decline, the stock is now valued at 3.8 times forward price-to-sales, or $13.21 per share. Is this an attractive entry point? to make an informed decision.

Other Stocks Worth Considering

ALSO RECOMMENDED: Top 5 Momentum Stocks. The ideal time to invest in a standout stock is when it’s gaining market attention. These companies not only have strong fundamentals but are also experiencing significant momentum right now.

Discover which stocks our AI-driven platform is highlighting this week. View the current list of Strong Momentum stocks—completely free. .

Our selections have included well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Comfort Systems, which delivered a 782% return over five years. .

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Howmet Aerospace: A Look at the Real Business Behind the 800% Run

Oil prices are climbing rapidly—causing concern among stock market investors. This is the reason behind it.

BCP Investment: Fourth Quarter Earnings Overview

Uber Shares Drop 1.58% Amid Mixed Market as 1.36B-Share Volume Ranks 91st