Howmet Aerospace: A Look at the Real Business Behind the 800% Run

Let's kick the tires on Howmet's story. The numbers look great on paper: full-year revenue grew 11% to $8.3 billion last fiscal year, with Commercial aerospace up 12% and Defense up 20%. That's a solid run. But the real test is whether the parking lot at the factory is full, and whether the planes in the sky are actually flying enough to need all these parts.

The evidence points to yes, for now. The company's confidence is tangible. In December, it announced it was acquiring Consolidated Aerospace Manufacturing for approximately $1.8 billion. That's not a move for a shrinking market. It's a bet on long-term demand for precision fasteners, the kind of parts that hold giant jet engines together. Management called it a "major step" to build out its portfolio. In other words, they're buying capacity and capability because they see the orders coming.

And the orders are there. The global engine market is humming. The International Air Transport Association projects global passenger traffic will hit a record 5.2 billion in 2026. That's a lot of people flying, which means airlines are ordering more planes and keeping their fleets busy. That directly fuels demand for the jet engines and the maintenance parts HowmetHWM-- supplies. The backlog at Boeing and Airbus is massive, taking over a decade to deliver. That's a long runway for suppliers.

So the common-sense story checks out. Strong travel demand → more planes ordered and flying → more engines built and maintained → more need for Howmet's specialized components. The 13% growth in Commercial aerospace last quarter and the 20% jump in Defense are backed by this real-world utility. The stock's 800% run isn't just hype; it's a reflection of this durable demand.

Yet, that's exactly the problem. The valuation now prices in perfection. The business is strong, but the stock's extreme move leaves no room for a stumble. If the passenger growth forecast slips, or if an engine order gets delayed, the story could unravel fast. For now, the parking lot is full. But the market is already paying for a full lot for years to come.

The Financial Engine: Quality of Growth and Profitability

The numbers here are impressive, but the real story is in the quality of the cash and the efficiency of the engine. Let's do a quick smell test.

First, the operational leverage is undeniable. In the fourth quarter, adjusted EBITDA jumped 29% year-over-year to $653 million. That's a powerful beat against the top-line growth of 15%. It means for every dollar of new sales, the company is keeping a much bigger chunk in its pocket. The adjusted EBITDA margin expanded by over 3 percentage points. That's the hallmark of a business model getting more efficient, not just bigger.

Then there's the cash. The company didn't just report profits; it generated real money. In that same quarter, cash from operations hit $654 million. That's the lifeblood of any business. And the company used a chunk of it to reward shareholders, repurchasing $200 million of its own stock. That's a clear vote of confidence from management, saying the stock is undervalued and the cash is better in shareholders' hands than sitting idle.

| Total Trade | 0 |

| Winning Trades | 0 |

| Losing Trades | 0 |

| Win Rate | 0% |

| Average Hold Days | 0 |

| Max Consecutive Losses | 0 |

| Profit Loss Ratio | 0 |

| Avg Win Return | 0% |

| Avg Loss Return | 0% |

| Max Single Return | 0% |

| Max Single Loss Return | 0% |

So the financial engine runs well. But here's the skeptical twist: the market is now paying a premium for this perfection. The stock trades at a price-to-earnings ratio of 70.35. That's not a valuation for a solid, growing business. That's a valuation for a flawless one. It assumes the 29% EBITDA growth and the 40% EPS expansion will continue year after year without a hitch.

The bottom line is that the quality of the earnings is high-strong margins, robust cash flow, and a disciplined return of capital. But the price you pay for that quality is extreme. The market is pricing in near-perfect execution, leaving no room for a stumble in demand, a margin pressure from materials, or a delay in those massive engine orders. For now, the engine is firing on all cylinders. But at a P/E of 70, you're paying for a flawless engine that never needs maintenance.

The Risks and What to Watch: Guardrails for the Run

The 800% run has created a fragile setup. The business is strong, but the stock now trades at a price-to-earnings ratio of 70.35. That's a valuation that assumes perfection. The primary risk is simple: a slowdown in aerospace demand or any compression in those razor-thin margins could pressure the stock sharply. The market is paying for flawless execution, not a single misstep.

The near-term operational focus is the $1.8 billion acquisition of Consolidated Aerospace Manufacturing (CAM). This is a major step, but it's also a test. The company expects CAM to generate about $490 million in revenue next year. The real question is whether the promised synergies and the significant tax benefit can deliver the promised returns. Integration is never clean, and any stumble here would be a direct hit to the premium paid.

Investors should watch for updates on the 2026 revenue guidance of approximately 10% growth. That's the baseline. Any signal that this is slipping, especially if it's tied to a delay in those massive engine orders, would be a red flag. Equally important is any clarity on defense budget stability. The company's Defense segment grew 20% last year, but that growth is tied to government spending. If that funding shifts, it could quickly change the growth story.

The bottom line is that the guardrails are thin. The financial engine is powerful, and the demand story is real. But with a P/E over 70, the stock has no room for error. The next few quarters will be about proving that the CAM integration works and that the 10% growth target is not just a number, but a durable reality. Until then, the risk is that the parking lot full of orders gets a little emptier than expected.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

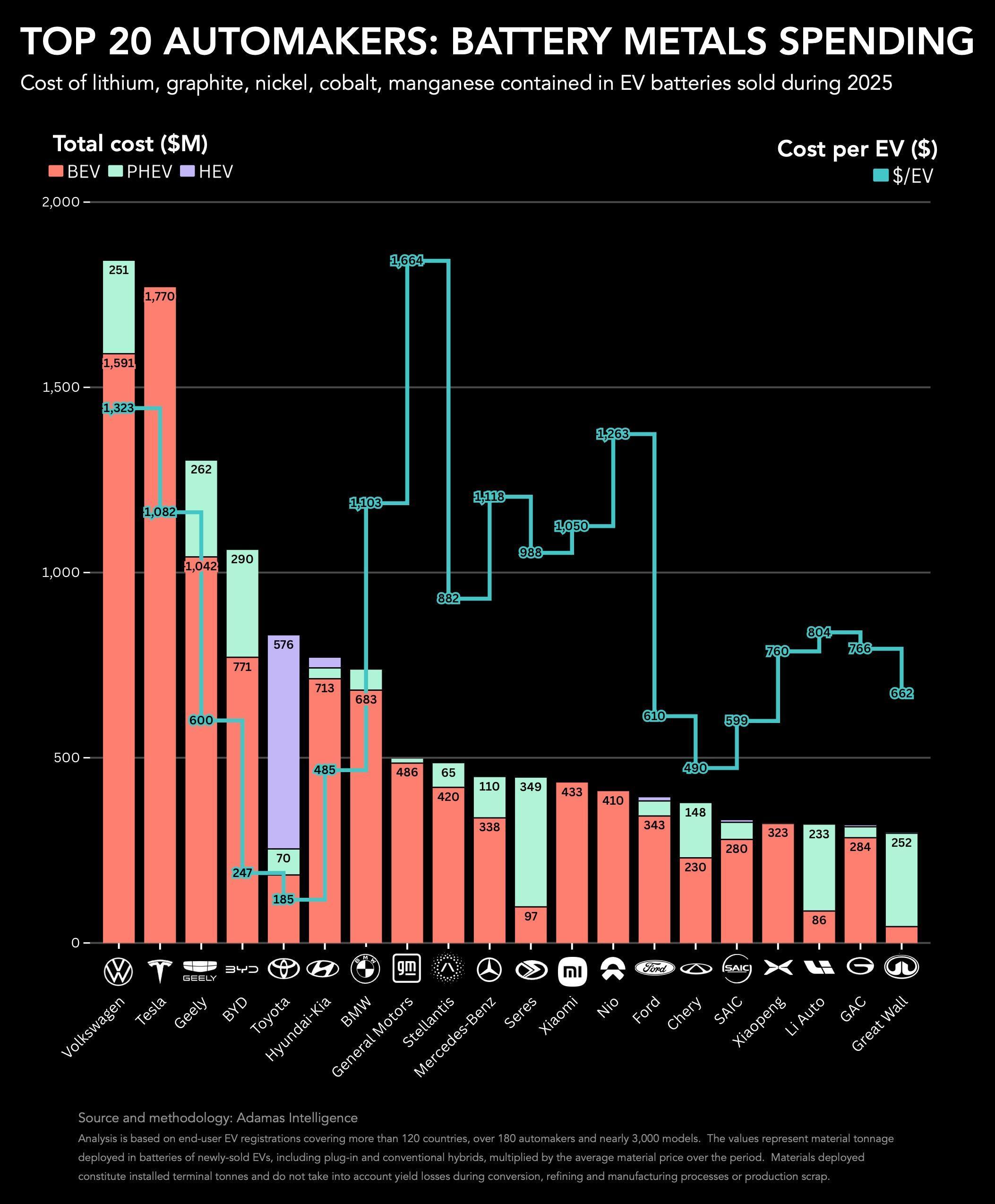

RANKED: Top 20 automakers by battery metals spending

China’s state iron ore buyer summons traders on BHP restrictions

BlockDAG’s Network Goes Live With Record-Breaking 100x Price Path! Hype Token Breaks Out & Worldcoin Faces Slump

HIVE's Two-Pronged Approach: Constructing the Foundation for AI Infrastructure