3 Motives to Offload BYRN and One Alternative Stock Worth Buying

Byrna Shareholders Face Tough Six Months

Investors in Byrna have endured a challenging half-year, with the stock price falling by 31.9% to its current level of $12.89. This significant drop may leave shareholders reconsidering their investment strategy.

Is Byrna now an attractive buy, or does it pose a threat to your portfolio?

Why We’re Not Enthusiastic About Byrna

Although the lower share price might seem appealing, we’re steering clear of Byrna for now. Below are three key reasons for our caution, along with a stock we prefer instead.

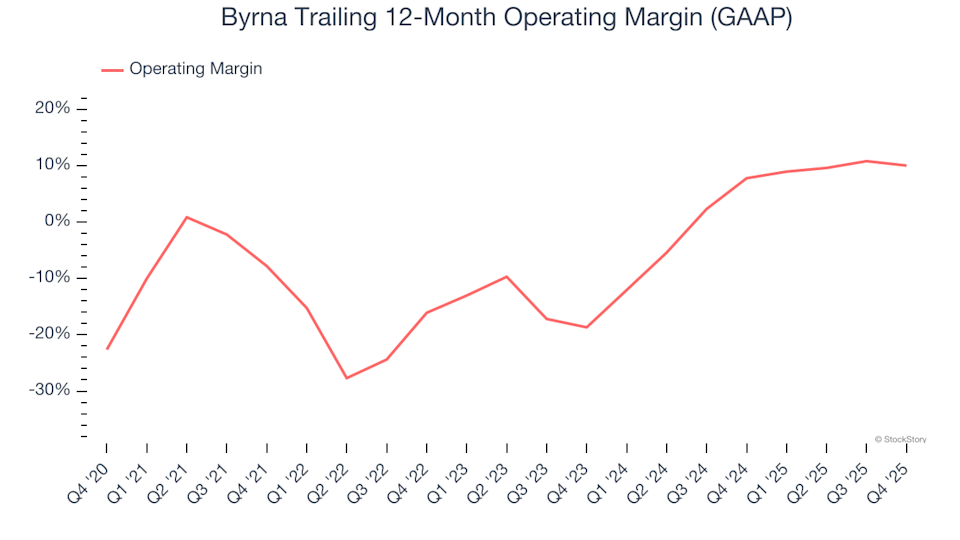

1. Operating Margins Offer Little Comfort

Operating margin is a crucial indicator of a company’s profitability, reflecting earnings before taxes and interest—factors that are less tied to core business performance.

Over the past five years, Byrna’s average quarterly operating profit has hovered around break-even, placing it among the weaker performers in the industrial sector.

Byrna Trailing 12-Month Operating Margin (GAAP)

2. Persistent Cash Burn Raises Red Flags

While free cash flow isn’t always front and center in financial statements, it’s a telling metric because it accounts for all operational and capital expenditures, making it difficult to obscure. In short, cash flow is vital.

Although Byrna managed to generate positive free cash flow in the latest quarter, its overall track record is less reassuring. Heavy reinvestment needs have depleted its cash reserves over the past five years, restricting its ability to reward shareholders. On average, Byrna’s free cash flow margin has been negative 6%, meaning it lost nearly $6 for every $100 in revenue.

Byrna Trailing 12-Month Free Cash Flow Margin

3. Limited Cash Reserves Could Lead to Dilution

For long-term investors, the greatest risk is a permanent loss of capital, which can occur if a company goes bankrupt or is forced to raise funds under unfavorable conditions. Short-term price swings are less concerning by comparison.

In the past year, Byrna used up $9.2 million in cash. With $15.48 million remaining on its balance sheet, and assuming its $2.35 million in debt isn’t immediately due, Byrna has about 20 months of financial runway left.

Byrna Net Cash Position

If Byrna’s fundamentals don’t improve soon, it may need to seek additional funding from investors to keep operating. Such a move could dilute existing shareholders, which is rarely good news for returns.

We remain wary of Byrna until it can consistently produce positive free cash flow or successfully execute its announced financing plans.

Our Verdict

While Byrna isn’t a fundamentally bad company, it doesn’t make our list of top picks. After its recent decline, the stock trades at a forward P/E of 27.4 (or $12.89 per share), which is a fair valuation. However, the company’s unstable financials introduce too much downside risk for our liking. We believe there are better opportunities in the market right now. Consider exploring one of our top-rated software stocks instead.

Top Stocks for Any Market Environment

WHILE YOU’RE HERE: Discover 9 Stocks That Consistently Outperform. The best-performing stocks don’t just beat the market once—they do it repeatedly. These companies show strong revenue growth, expanding free cash flow, and exceptional returns on capital. The market has already recognized their strength.

But according to our AI platform, their growth stories are far from over. See which 9 stocks made our list this week—completely free.

Our selections include well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Tecnoglass, which delivered a 1,754% return over five years. Find your next potential winner with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

AurumX Collaborates with FishWar to Redefine Web3-Based Gaming Economies

Solana processes 8x transactions more than BNB Chain – Details

MetaQuotes Begins Restricting Brokers Licensed in Comoros

Target expands next-day delivery service to an additional 20 cities