EXCLUSIVE: Why US, Iran War May Not Spark The Oil Crisis Everyone Fears

When war flares in the Middle East, and oil tankers start pausing their routes through the world’s most critical shipping chokepoint, the reflex is immediate: flashback to 2022 and the economic fallout of Russia’s invasion of Ukraine.

Energy prices soared, inflation spiraled and central banks scrambled to raise rates faster than at any point in decades.

But is that reflex justified this time? Benzinga put the question — and five others — to Bridget Payne, head of energy forecasting at Oxford Economics, one of the world’s leading independent economic research firms.

Her answers are striking for what they rule out as much as for what they flag as genuine risk.

Why This Isn't Another 2022 Energy Crisis — For Now

The energy shock that followed Russia's invasion of Ukraine in 2022 was driven by a sudden and structural loss of supply. When the Nord Stream pipelines shut down, a massive amount of natural gas disappeared from the market almost overnight — and markets had little reason to expect a quick recovery.

The current situation is different.

"What we are seeing now is largely a delay rather than a loss of supply," Payne told Benzinga.

Instead of a permanent loss of supply, energy flows are mainly being delayed.

Oil and gas tankers are pausing transit through the Strait of Hormuz due to rising insurance costs and security risks.

"As soon as it is safe enough to resume, those volumes can return to market. In other words, supply has largely been delayed rather than curtailed," Payne said.

That distinction matters.

Because supply is delayed rather than destroyed, global inventories can act as a buffer.

For a full inflation shock to emerge, Payne said disruptions would need to persist long enough to create genuine shortages.

What Would Push Oil Above $100?

A spike above $100 per barrel remains possible, but Oxford Economics does not see it as the base scenario.

"Yes, a long but partial disruption could push oil prices into triple digits if it lasted long enough to create shortages," Payne said.

A full and prolonged closure of the Strait of Hormuz would likely drive such a move.

However, even a moderate disruption could eventually push prices higher if it reduced supply for long enough.

Still, Payne said global powers have strong incentives to keep oil flowing.

President Donald Trump has suggested the U.S. could cover shipping insurance and provide military escorts for tankers moving through the region.

"Our expectation is that oil will find a way to keep flowing," Payne said.

Since the start of the war in Iran, the West Texas Intermediate light crude — as closely tracked by the United States Oil Fund (NYSE:USO) – has rallied by about 12% to $75 a barrel.

Spare Capacity As A Buffer

Another factor helping limit the risk of a severe supply shock is spare production capacity in the Gulf.

"We estimate that Saudi Arabia and the UAE have at least 3 mbpd of spare production capacity that can be utilised relatively quickly," Payne said.

In addition, U.S. shale production can respond relatively quickly to higher prices.

New wells can typically be drilled and completed within three to six months, allowing American output to increase in response to higher prices.

Together, those supply sources provide a buffer against lost Iranian production or broader disruptions in the Gulf.

Damage to energy infrastructure across the region remains possible but is not part of the base scenario.

Why Energy Infrastructure Is Being Targeted

Recent strikes affecting energy infrastructure appear aimed at raising the economic cost of the conflict.

"Strikes on energy infrastructure appear aimed at raising the economic cost of the conflict and increasing pressure on outside powers to respond," Payne said.

For energy markets, the key difference lies between disruptions to transit and disruptions to production.

Transit disruptions slow deliveries but do not necessarily remove supply.

Damage to production facilities, by contrast, would remove barrels from the market and could create longer-lasting shortages.

Payne said such damage remains a tail risk rather than the central case.

Europe Could Feel The Gas Impact First

If the conflict escalates, the gas market could feel the pressure unevenly. Europe remains more vulnerable because it relies heavily on liquefied natural gas cargoes to balance supply.

If Qatari shipments are disrupted, competition for available cargoes would intensify.

"The impact is likely to be felt much more in European than US gas prices," Payne said.

In the United States, liquefied natural gas export terminals are already operating near capacity. That limits how much additional global demand can tighten the domestic market.

As a result, Henry Hub prices — as tracked by the United States Natural Gas Fund LP (NYSE:UNG) — face less upside pressure than European benchmarks.

What About Inflation?

Second-round economic effects would likely appear first in transport costs.

Payne said a $10 increase in oil prices, if sustained, would add 28 cents to the retail price of regular gasoline in the United States.

Even with that increase, Oxford Economics expects only a modest inflation impact under its baseline outlook.

"Our baseline view is that the impact on inflation in the US and Europe will be minor," Payne said.

More serious spillovers would require disruptions that create genuine supply shortages. Only then would central banks likely reconsider plans to cut interest rates.

The key variable in 2026 compared to 2022 is time. A brief disruption, even a severe one, is something analysts argue markets can absorb. A prolonged one — particularly if it involves sustained damage to production infrastructure rather than transit delays — is a different story altogether.

Image: Shutterstock

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Cross Country: Fourth Quarter Financial Results Overview

Enhabit: Fourth Quarter Financial Overview

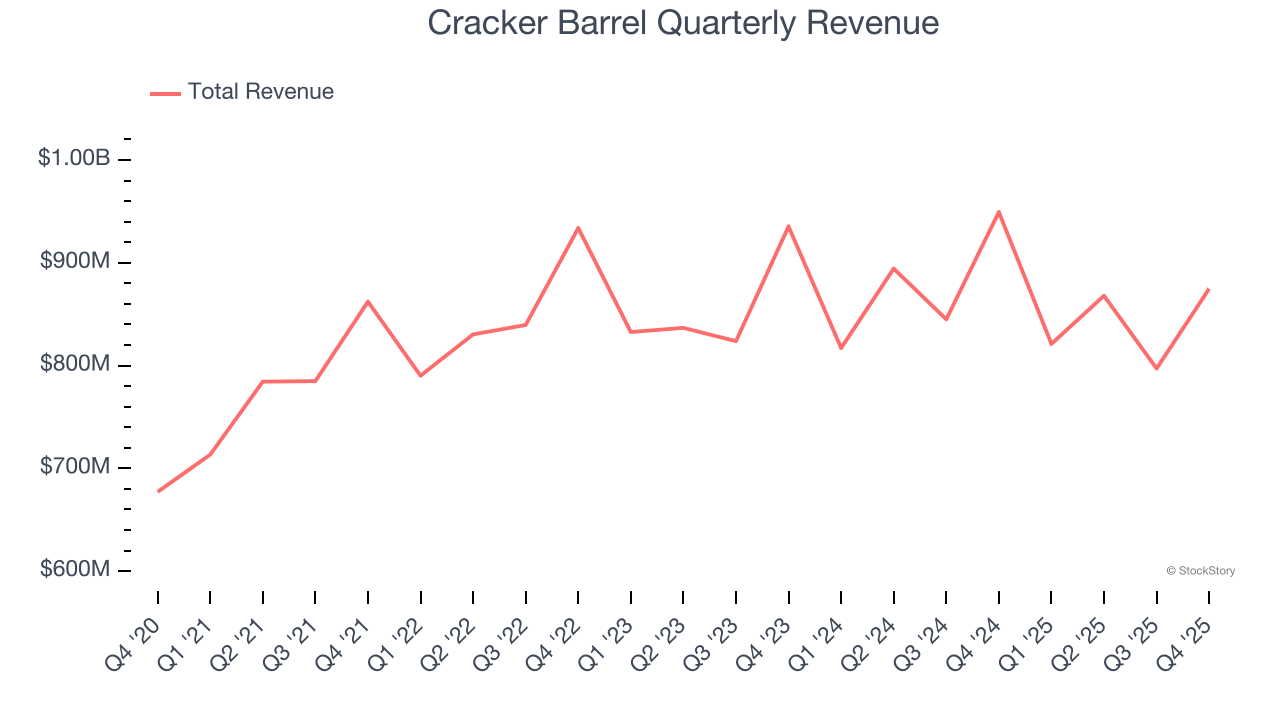

Cracker Barrel's (NASDAQ:CBRL) Q4 CY2025 Sales Top Estimates, Stock Soars

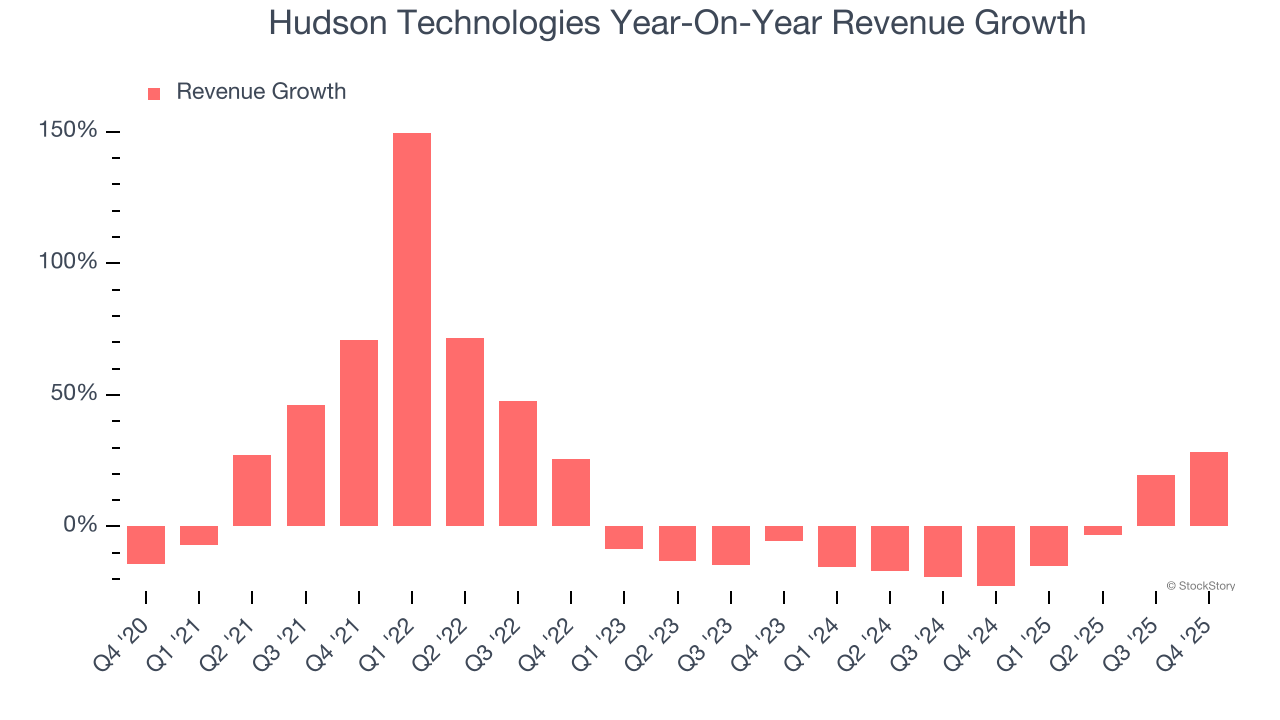

Hudson Technologies (NASDAQ:HDSN) Surprises With Q4 CY2025 Sales