Iran conflict disrupts the popular approach of investing in Asia while reducing exposure to the United States

Asian Markets Face Turbulence Amid Iran Conflict

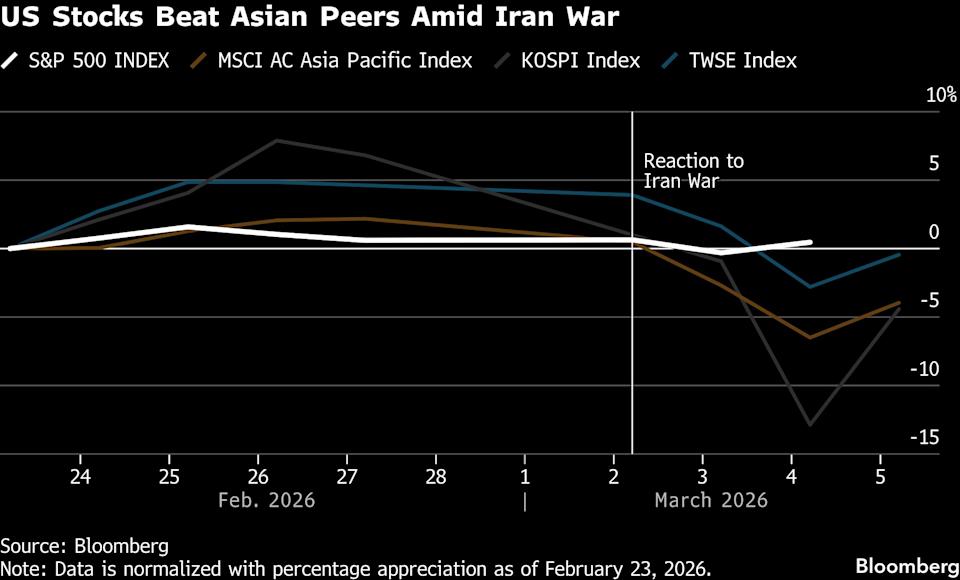

The ongoing conflict in Iran has prompted investors to reconsider their strategies, with many now questioning the effectiveness of the once-popular “Sell America, Buy Asia” approach. This shift comes as Asian equities experience significant volatility, marking a potential turning point for global market trends.

Market Performance Diverges

This week, the MSCI Asia Pacific Index has dropped roughly 6%, while the S&P 500 has seen only a marginal decline of 0.1%. This stark contrast signals a reversal in the flow of international capital, with funds moving back toward the perceived safety of US assets, further supported by a strengthening US dollar.

Asian Stocks Under Pressure

Asian equities have been hit particularly hard due to the region’s heavy dependence on energy imports passing through the Strait of Hormuz. Fears of a prolonged supply disruption are raising concerns about a potential global slowdown, which could hurt major export sectors. Investors are now locking in profits from the recent AI-driven surge, especially in markets like South Korea and Taiwan that have outperformed over the past year.

“Capital is already on the move, and the dollar’s rally this week reveals where investors see safety,” explained Hebe Chen, a senior analyst at Vantage Global Prime. “Countries like China, Japan, Korea, and Taiwan, which rely heavily on energy imports, are especially vulnerable to this oil shock compared to Western economies.”

Previously, Asian stocks were attractive for their exposure to AI hardware, appealing valuations, and robust earnings growth.

Rising Oil Prices and Inflation Risks

The recent surge in Brent crude prices is fueling inflation concerns, threatening to turn Asia’s strengths into weaknesses. Even as markets attempted a rebound, oil prices continued their upward trend for a fifth consecutive day, despite reassurances from US President Donald Trump regarding the ongoing military operations.

“Stagflation is the biggest threat to the AI investment story—when borrowing costs rise and growth prospects dim, ambitious infrastructure projects become difficult to justify,” noted Chen from Vantage.

According to Bloomberg Economics, major Asian economies such as China, India, and Indonesia are among the world’s largest oil importers. Goldman Sachs projects that a 20% increase in Brent crude could reduce regional corporate earnings by 2%.

Regional Vulnerabilities

Japan and South Korea are particularly exposed to disruptions in shipping routes, unlike China, which benefits from larger reserves and access to Russian oil. In response to supply risks, Beijing has instructed its top refiners to halt exports of diesel and gasoline.

“Japan and South Korea are especially at risk, as over 60% of their oil imports pass through the Strait of Hormuz,” said Alicia Garcia-Herrero, chief Asia Pacific economist at Natixis SA. She emphasized that the economic impact extends beyond oil, affecting transportation, construction, finance, and defense sectors.

Comparative Impact: Asia vs. US

Persistently high oil prices could reshape the outlook for Asian equities by tightening financial conditions and weakening external balances. In contrast, the US is more insulated due to its role as an energy exporter and its appeal as a safe haven, according to Amundi Investment Institute. DWS also expects Europe and Asia to feel the brunt of these shocks more than the US, given America’s fuel production capabilities.

“The Strait of Hormuz is crucial, but the US is not heavily reliant on Middle Eastern oil,” said Ajay Rajadhyaksha, global research chairman at Barclays, in a Bloomberg TV interview. “The situation is far more critical for Europe and, most importantly, for major Asian economies like China, South Korea, and Japan.”

Currency and Policy Shifts

Investors are drawing parallels to 2022, as market reactions mirror those seen after Russia’s invasion of Ukraine, including a stronger dollar. A rising dollar puts pressure on Asian currencies, limits the ability of central banks to ease monetary policy, and clouds the outlook for corporate profits.

This week, Bloomberg’s dollar index has climbed 1.4%, on track for its largest weekly gain since November 2024, while a similar index for Asian currencies has fallen 0.9%. Traders now anticipate about 50 basis points of rate hikes from the Bank of Korea over the next year, up from 25 basis points expected just weeks ago.

“The absence of monetary easing will weigh on equities,” said Rajeev de Mello, global macro portfolio manager at Gama Asset Management. “Optimism among emerging market investors could also fade.”

Momentum Unwinds, But Optimism Remains

Despite Thursday’s rebound, which highlights how quickly sentiment can change, many investors remain positive about the long-term prospects for Asian stocks. UBS Global Wealth Management recently upgraded South Korean equities, arguing that the recent correction and volatility were technical in nature rather than a sign of weakening fundamentals.

“Unless tensions in the Middle East escalate further—which seems unlikely for now given recent US and Israeli actions—we expect Asian markets to maintain their upward momentum,” said Jon Withaar, portfolio manager at Pictet Asset Management in Singapore. He pointed to Japan’s economic reforms, South Korea’s corporate governance changes, and the global shortage of memory chips as potential drivers of future gains.

However, even without broader macroeconomic threats, Asian equities remain susceptible to risk-off moves, especially after their recent outperformance against US stocks. Foreign investors withdrew $6.3 billion from Taiwanese equities in the first three days of the week, setting the stage for one of the largest weekly outflows on record.

In 2025, the MSCI Asia Pacific Index outpaced the S&P 500 by the widest margin since 2017. Despite the recent downturn, it still leads the US by 7 percentage points this year, suggesting there is room for further unwinding of crowded positions.

“Asia’s current selloff is the result of multiple factors, not just geopolitical risks,” said Elfreda Jonker, client portfolio manager at Alphinity Investment Management. “Markets like South Korea are particularly exposed right now due to their recent strong performance and high valuations.”

©2026 Bloomberg L.P.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.