Why Trump Prefers Magnets Over Gold

U.S. Military to Ban Chinese Rare Earth Magnets by 2027

Starting in 2027, the U.S. Department of Defense will enforce a ban on the use of rare earth magnets sourced from China in American military equipment.

This new regulation requires defense manufacturers to thoroughly trace and verify the origins of rare earth metals used in their products, ensuring transparency throughout the entire supply chain.

Major defense contractors, including Lockheed Martin, are restructuring their magnet sourcing processes to comply with the upcoming rules. They emphasize the need for full traceability, from mining to finished product, across all supplier levels. Northrop Grumman has also issued new supplier guidelines to reinforce these requirements throughout its network.

These industry leaders are now seeking qualified suppliers in a market where China has long dominated rare earth processing.

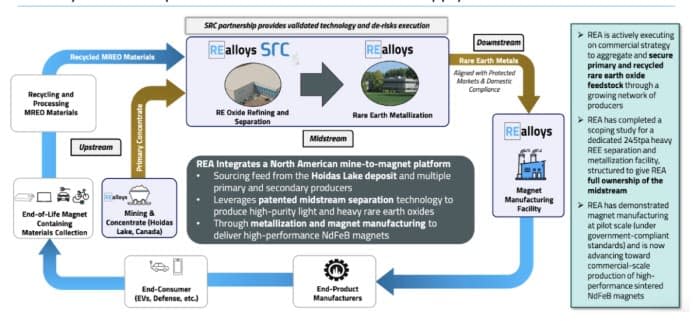

In Euclid, Ohio, the landscape is shifting. REalloys (NASDAQ: ALOY) has become the first North American company to produce heavy rare earth metals suitable for defense-grade magnets at an industrial scale.

Securing Magnet-Grade Metals for Defense

At Mountain Pass, rare earth concentrate is processed in California to produce NdPr oxide, marking progress in rebuilding domestic capabilities. However, defense applications require the oxide to be further refined into pure metal, which is then alloyed for magnet production.

For years, the critical step of converting oxide to metal has been almost entirely performed in China—even when the raw materials originated in the U.S. This overseas dependency has been the weak link in the supply chain.

REalloys is working to close this gap.

The North American supply chain now follows this structure:

- Supply chain security and control begin upstream.

- REalloys owns the Hoidas Lake rare earth project in Saskatchewan, ensuring Canadian resource access.

- In Greenland, a long-term agreement covers about 15% of future output from the Tanbreez project, one of the largest non-Chinese rare earth deposits.

- Agreements in Kazakhstan and Brazil add further non-Chinese sources of supply.

Expanding Domestic Processing Capacity

In addition to primary mining sources, REalloys supplements its feedstock with recycled magnets and industrial scrap. All materials are processed and refined in North America, culminating in metallization at the Euclid facility.

Euclid is now operating at industrial scale, tackling the most challenging step in the rare earth supply chain.

“Metallization is the least developed segment outside China. It demands extensive expertise and advanced process controls to manage complex, continuous production. Even with investment and strong execution, building this capability typically takes three to seven years or more, with significant technical and qualification risks,” explains REalloys co-founder Tim Johnston.

He adds, “We have already overcome the toughest challenge—demonstrating that rare earth metallization and alloying can be achieved domestically to meet real-world customer standards.”

REalloys (NASDAQ: ALOY) is now closing the loop from mine to finished magnet, just as the U.S. prepares to restrict Chinese-sourced defense materials.

Meeting National Security Deadlines

Production capacity is ramping up to meet a critical national security timeline. REalloys and SRC aim to produce around 400 tonnes of rare earth metal annually by the end of 2027, with plans to increase to 600 tonnes as operations expand. This aligns with the compliance deadlines for U.S. defense contractors.

The addition of retired General Jack Keane to the board underscores the strategic importance of domestic rare earth metallization. As a former Vice Chief of Staff of the U.S. Army, Keane brings high-level expertise in military readiness and procurement, highlighting that oxide-to-metal conversion is now a key factor in defense planning.

Federal funding is following suit. The Export-Import Bank has expressed interest in providing up to $200 million for rare earth processing expansion, and the Defense Production Act offers further support for boosting domestic capacity.

This is no longer just about commodities; it is a capital-intensive, deadline-driven overhaul of the defense supply chain. Companies specializing in metallurgical processes will play a pivotal role in this transition.

Critical Role of Metallization in Defense Manufacturing

Rare earth elements enter defense manufacturing only after being refined into high-purity metals and alloyed for magnet applications. This crucial step determines whether advanced weapon systems can be produced and deployed reliably and on schedule. REalloys, in partnership with SRC, is leading this effort in Euclid, Ohio.

If North America and its allies fail to rebuild this segment of the supply chain, the U.S. military would remain reliant on China for essential materials.

Production timelines for missiles, aircraft, and naval systems are governed by rigorous certification and traceability standards that take years to establish.

In times of crisis, such as potential military action in the Middle East, the Pentagon cannot risk delays caused by material shortages.

Scaling Up Before the Ban Takes Effect

The initial phase restored a lost capability to North America. The next phase focuses on expanding and financing it.

REalloys has already demonstrated that North America can independently convert rare earth oxides into valuable metals. The company is now scaling up, with the Euclid facility serving as the foundation for a broader processing network that extends from secure raw materials to finished magnets.

The distinction between a single facility and a full-scale platform lies in throughput.

Phase 1 is already operational, with Euclid producing rare earth metals today. The current goal is to reach about 400 tonnes per year by the end of 2027, increasing to 600 tonnes as production stabilizes. This includes key heavy rare earths like dysprosium and terbium for high-temperature magnets, as well as NdPr for permanent magnet strength.

Given the limited global supply of heavy rare earths outside China, these volumes make Euclid one of the few significant production sites in North America.

Engineering, site development, and plant construction will continue through 2026 and 2027, with the goal of capturing more value within allied territories.

Significant capital is now committed to this expansion.

The Export-Import Bank’s interest in providing up to $200 million in financing supports the growth of rare earth processing linked to this platform. The Defense Production Act offers additional funding channels as capacity increases. Both financial structure and industrial policy are aligned toward this goal.

The next phase will be defined by plant expansions, financing milestones, engineering achievements, and increased output.

REalloys is now entering a period of significant growth.

By Michael Kern

The AI Revolution and Energy Demand

The rapid rise of artificial intelligence is fueling an unexpected surge in demand for natural gas and energy stocks. Those overlooking the energy needs of data centers risk missing out on the decade’s most significant energy trend. Savvy investors are already positioning themselves in companies poised to supply the trillion-dollar AI industry.

Oilprice Intelligence offers expert insights into where the next big opportunities lie, with analysis from seasoned professionals in the oil sector.

Disclosures and Notices

- Disclosure: The owner of Oilprice.com holds shares and/or stock options in the featured company and may benefit from its performance. Please conduct your own research and consult a financial advisor before investing.

- Forward-Looking Statements: This publication contains projections and expectations about future growth. Actual results may differ due to various risks and uncertainties, including regulatory changes, market size, funding, and pricing pressures.

- Disclaimer: Neither the author nor Oilprice.com received compensation for this communication about REalloys (NASDAQ: ALOY). The owner of Oilprice.com may buy or sell shares at any time, which could present a conflict of interest. Readers are urged to perform thorough due diligence and consult with a financial professional before making investment decisions. This communication is not an offer to buy or sell securities and should not be considered personalized investment advice. Investing in securities carries significant risk, and past performance does not guarantee future results.

- Indemnification: By reading this communication, you acknowledge and accept this disclaimer and release the publisher and its affiliates from any liability. You are solely responsible for your investment decisions.

- Terms of Use: By continuing to read, you agree to the Terms of Use of Oilprice.com. If you do not agree, please contact Oilprice.com to unsubscribe.

- Intellectual Property: Oilprice.com is a trademark of the publisher. All other trademarks belong to their respective owners. The publisher is not affiliated with or endorsed by these trademark holders unless stated otherwise.

Stay Ahead with Oilprice Intelligence

Oilprice Intelligence delivers market-moving insights before they hit the headlines. This expert analysis is trusted by seasoned traders and policymakers. Subscribe for free to receive timely updates and understand the forces driving the market.

Gain access to geopolitical analysis, exclusive inventory data, and insider information that influences billions in market value. Receive $389 worth of premium energy intelligence at no cost—join over 400,000 readers today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

DXY Retest at 99.183: Will 100–101 Break as US Degen Index Stabilizes?

RBA's Hauser: Regarding the US Dollar's Role as a Safe Haven

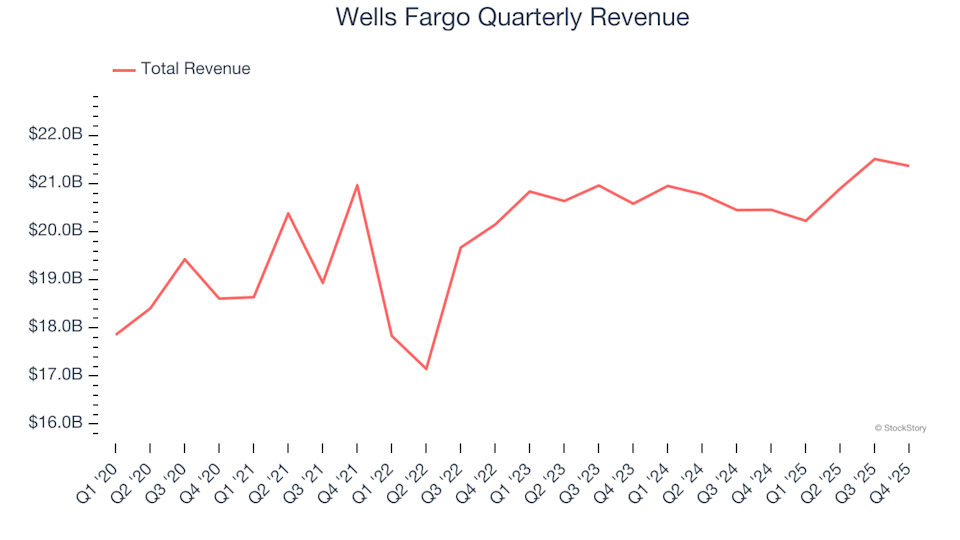

3 Reasons to Steer Clear of WFC and One Alternative Stock Worth Buying

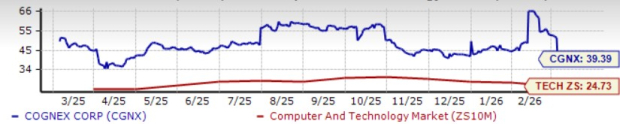

Can AI Initiatives & Improving Margins Drive Cognex Shares in 2026?