Freeport-McMoRan's Stock Surges 39% Over Three Months: What's the Best Way to Invest?

Freeport-McMoRan Inc. Sees 39% Stock Surge Amid Rising Copper Prices

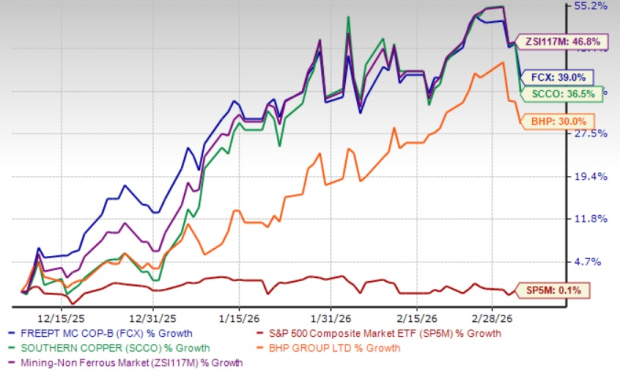

Over the past quarter, shares of Freeport-McMoRan Inc. (FCX) have soared by 39%, fueled by a rally in copper prices. This growth has been supported by concerns over limited global supply, ongoing trade uncertainties, and robust demand. While Freeport's performance trailed the Zacks Mining - Non Ferrous sector's 46.8% gain, it still outpaced the S&P 500, which edged up just 0.1% in the same timeframe. In comparison, Southern Copper Corporation (SCCO) and BHP Group Limited (BHP) posted gains of 36.5% and 30%, respectively.

Three-Month Stock Performance

Image Source: Zacks Investment Research

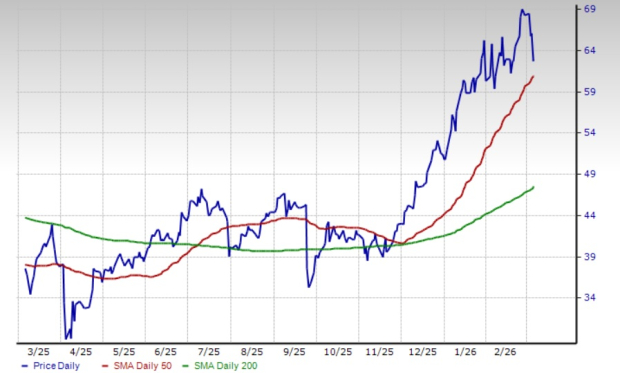

Since late November 2025, FCX shares have consistently traded above both their 50-day and 200-day simple moving averages (SMA). A bullish "golden cross" occurred on July 8, 2025, when the 50-day SMA moved above the 200-day SMA, signaling positive momentum for the stock.

FCX Stock and the 50-Day SMA

Image Source: Zacks Investment Research

To better understand FCX’s outlook, let’s examine its core business fundamentals.

Expansion Initiatives Set to Drive Future Growth

Freeport is capitalizing on its portfolio of high-grade copper assets, focusing on disciplined management and organic growth to enhance output. At the Cerro Verde mine in Peru, a major concentrator expansion has added about 600 million pounds of copper and 15 million pounds of molybdenum to annual production. The company has also completed an assessment for a large-scale expansion at El Abra in Chile, targeting a significant sulfide resource that could support a new mill project, similar in scale to Cerro Verde, with an estimated 20 billion pounds of recoverable copper.

In Arizona, FCX is advancing pre-feasibility studies at its Safford/Lone Star sites, aiming to complete them by 2026 and evaluate a substantial sulfide expansion. At the Bagdad operation, expansion plans could more than double current concentrator capacity, with studies indicating the potential to boost copper output by 200–250 million pounds annually.

In Indonesia, PT Freeport Indonesia (PT-FI) finished constructing a new greenfield smelter in Eastern Java in 2024, with operations starting in the second quarter of 2025 and the first copper anode produced in July 2025. PT-FI is also developing the Kucing Liar ore body in the Grasberg district, targeting a production ramp-up by 2030. Studies completed in 2025 revealed an opportunity to increase Kucing Liar’s design capacity to 130,000 metric tons of ore per day and expand reserves by about 20% at low cost. Additionally, gold production commenced at a new precious metals refinery in late 2024.

Strong Financial Position and Capital Management Support Growth

FCX maintains a robust liquidity position and generates significant cash flow, enabling it to fund expansion, reduce debt, and return value to shareholders. In 2025, the company reported operating cash flows of approximately $5.6 billion, including $693 million in the fourth quarter. By year-end, Freeport held around $3.8 billion in cash and equivalents, $3 billion available through its revolving credit facility, and $1.5 billion via the PT-FI credit facility.

Net debt stood at $2.3 billion at the end of 2025, excluding new downstream facilities at PT-FI, which is below the company’s target range of $3–$4 billion. Freeport’s policy allocates half of available cash to shareholders, with the remainder used for debt reduction or growth investments. The company faces no major debt maturities until 2027, and its long-term debt-to-capitalization ratio is about 22.5%, lower than Southern Copper’s 37.8% and BHP Group’s 30.7%.

FCX currently offers a dividend yield of roughly 0.5%, with a payout ratio of 17%—well below the 60% threshold that typically signals dividend sustainability. The company’s strong financial health supports the reliability of its dividend payments.

Favorable Copper Market Trends Benefit Freeport

Copper prices, essential for the electrification sector, were volatile but generally strong throughout the previous year, staying above $5 per pound in the fourth quarter of 2025. The start of 2026 saw copper prices remain elevated, driven by strong demand from China and the U.S. Ongoing trends such as electric vehicle adoption, renewable energy projects, data center expansion, and grid upgrades continue to fuel copper consumption.

Concerns about supply constraints, especially with rising demand from EVs and infrastructure projects, have kept copper prices near $6 per pound. Freeport’s average realized copper price rose by about 28% year-over-year to $5.33 per pound in the fourth quarter, and continued strong pricing is expected to support the company’s performance going forward.

Rising Costs Pressure FCX Margins

Despite positive market trends, Freeport is contending with increased costs. In the fourth quarter of 2025, the company’s average unit net cash cost per pound of copper jumped to $2.22 from $1.40 in the previous quarter—a 59% increase—and was up 34% year-over-year, largely due to lower copper sales volumes.

Looking ahead to the first quarter of 2026, FCX anticipates further cost increases, projecting unit net cash costs to reach $2.60 per pound and a full-year average of about $1.75. Lower expected sales volumes are likely to keep costs elevated, which could put additional pressure on margins.

Reduced Sales Volumes Impact Outlook

In the fourth quarter, Freeport’s copper sales volumes dropped by roughly 29% year-over-year to 709 million pounds, down from 977 million pounds in the prior quarter. Gold sales also fell sharply, declining about 77% year-over-year to 80,000 ounces. These declines were mainly due to a temporary halt in operations following a mud rush incident at the Grasberg Block Cave mine in Indonesia in September 2025.

For the first quarter of 2026, Freeport expects minimal contribution from its Indonesian operations, forecasting copper sales volumes of 640 million pounds—a 10% sequential and 27% annual decrease. Gold sales are projected at 60,000 ounces, also reflecting declines. These lower volumes are expected to weigh on revenue in the near term. However, the company is preparing for a phased restart of the Grasberg Block Cave underground mine beginning in the second quarter of 2026.

Upward Revisions in Earnings Estimates

Analyst expectations for Freeport’s earnings have improved over the past two months, with the Zacks Consensus Estimate for both 2026 and 2027 being revised higher during this period.

Image Source: Zacks Investment Research

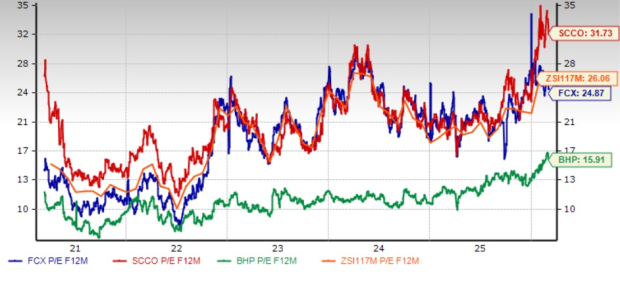

Valuation Overview

FCX currently trades at a forward price-to-earnings ratio of 24.87, representing a 4.6% discount to the industry average of 26.06. The stock is valued below Southern Copper but above BHP Group.

FCX’s Forward P/E Compared to Industry Peers

Image Source: Zacks Investment Research

Conclusion: Maintain Positions in FCX

Freeport is well-positioned to benefit from its ongoing expansion projects, which should enhance production capabilities. Its solid financial footing allows for continued investment in growth while supporting shareholder returns. Upward-trending earnings estimates and favorable copper prices are positive factors. However, the outlook is tempered by lower projected sales volumes and rising costs. Investors currently holding this Zacks Rank #3 (Hold) stock may consider maintaining their positions.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Nvidia Releases Financial Results. Investors on Wall Street Respond, "Is That All?"

Patrick Bet-David’s Bombshell XRP Price Forecast if XRP Captures 5% of SWIFT Volume

The new American AI restrictions cause Nvidia stock to plunge