Should You Steer Clear of QCOM Shares as Estimate Revisions Drop?

QCOM Earnings Outlook Weakens

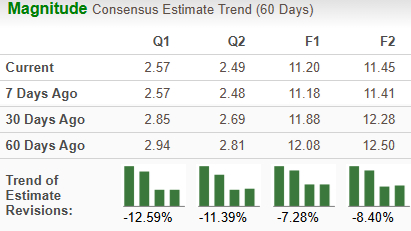

Over the past two months, analysts have lowered their earnings projections for Qualcomm Incorporated (QCOM) for fiscal years 2026 and 2027 by 7.3% and 8.4%, respectively, now forecasting $11.20 and $11.45 per share. These downward revisions reflect growing pessimism about the company’s future growth prospects.

Image Source: Zacks Investment Research

Challenges Facing Qualcomm

Qualcomm’s expansion in China has been hampered by ongoing trade tensions between the United States and China. With operations in over a dozen Chinese cities and a history of supplying chips to major smartphone brands such as Xiaomi, Huawei, and Honor, the company now finds it increasingly difficult to sustain its business in the region. U.S. government restrictions on the export of advanced technology and components to China have intensified, while China has accelerated efforts to build its own semiconductor industry. This dual pressure has created both regulatory hurdles and heightened competition from domestic chipmakers for Qualcomm. Additionally, reduced consumer and business spending in China has led to higher inventory levels among customers, further impacting demand.

Demand Headwinds Impacting Performance

Short-term demand for Qualcomm’s products is expected to remain subdued. For the second quarter of fiscal 2026, the company anticipates GAAP revenue between $10.2 billion and $11 billion, with handset revenue around $6 billion. This is attributed to lower chip orders and ongoing uncertainty in memory supply and pricing for handset manufacturers. Many Chinese OEMs are scaling back on new 4G device purchases and managing inventory ahead of the shift to 5G, which is likely to result in lower device shipments as inventory levels are adjusted throughout the supply chain.

Profit Margins Under Pressure from R&D Spending

Qualcomm’s profit margins have been squeezed by rising operating and research and development expenses. The company expects continued weakness in the handset market and a less favorable product mix in the near term. Shifts among leading device manufacturers, especially in the premium segment, have also reduced opportunities to sell integrated Snapdragon chipsets.

Competition remains fierce, with rivals such as Broadcom and Hewlett Packard Enterprise intensifying the pressure. The influx of low-cost chipmakers and established competitors in the mobile chipset space is likely to further erode Qualcomm’s profitability. While global smartphone sales are projected to grow over the next several years, much of this expansion is expected to come from emerging markets where lower prices may compress margins.

Image Source: Zacks Investment Research

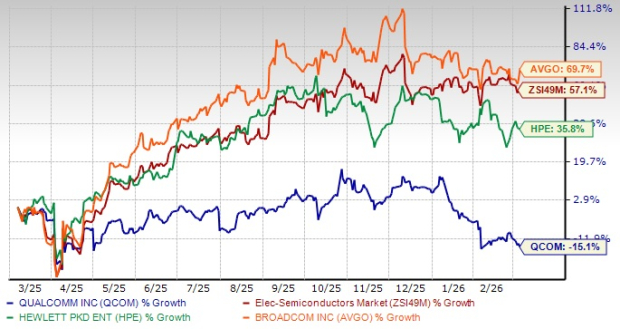

Stock Performance Comparison

In the past year, Qualcomm’s share price has fallen by 15%, significantly underperforming the broader industry, which has surged by 57.1%. Competitors like Hewlett Packard Enterprise (HPE) and Broadcom Inc. (AVGO) have seen their stocks rise by 35.8% and 69.7%, respectively, during the same period.

QCOM One-Year Stock Price Trend

Image Source: Zacks Investment Research

Strategic Focus: Snapdragon and Automotive Expansion

Despite current challenges, Qualcomm is betting on growth in mobile and automotive sectors, leveraging its Snapdragon platform. These processors offer advanced features, high performance, and strong security, making them attractive for mobile devices worldwide. The company is also expanding into AI-powered laptops and desktops with the introduction of the Snapdragon X chip.

In the automotive space, Qualcomm has strengthened its position in vehicle-to-everything (V2X) communications through the acquisition of Autotalks. This move enables Qualcomm to deliver a comprehensive range of automotive-grade V2X solutions for cars, motorcycles, and roadside infrastructure.

Conclusion

Qualcomm stands to benefit from its investments in automotive technologies and the Snapdragon platform, supported by a focus on quality and ongoing product innovation. However, declining earnings forecasts, intense competition, and weak demand in key markets are weighing on the company’s outlook. High research and development costs continue to impact profitability, and the company faces a challenging environment in China due to trade barriers and reduced chip orders. Given these headwinds, investors may want to exercise caution regarding Qualcomm stock at this time.

Qualcomm currently holds a Zacks Rank #5 (Strong Sell).

For a full list of Zacks #1 Rank (Strong Buy) stocks, click here.

Zacks Research: Top Stock Picks

Zacks’ research team has identified five stocks with the potential to double in value in the coming months. Among these, the Director of Research, Sheraz Mian, has spotlighted a satellite communications company poised for rapid growth as the space industry expands toward a trillion-dollar market. Analysts expect a significant revenue surge for this company in 2025. While not every top pick is guaranteed to succeed, this stock could outperform previous winners like Hims & Hers Health, which soared over 200%.

- Qualcomm Incorporated (QCOM): Free Stock Analysis Report

- Broadcom Inc. (AVGO): Free Stock Analysis Report

- Hewlett Packard Enterprise Company (HPE): Free Stock Analysis Report

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Breaking: Iran says no more attacks against neighbouring countries “unless they attack first”

Pundit Describes How $10,000 In XRP Could Become $1,000,000

Nvidia Releases Financial Results. Investors on Wall Street Respond, "Is That All?"