Keysight (KEYS): Should You Buy, Sell, or Hold After Q4 Results?

Keysight’s Recent Surge: Should Investors Jump In?

Keysight Technologies has experienced a remarkable upswing, with its share price climbing 68.1% over the last half-year to reach $284.50. This impressive rally has been fueled in part by strong quarterly earnings, leaving many investors debating whether now is the right moment to buy or if caution is warranted.

Is this a good entry point for Keysight, or should you think twice before adding it to your holdings?

Why We’re Not Enthusiastic About Keysight

Despite the recent momentum, we’re choosing to stay on the sidelines. Here are three key reasons to be cautious about KEYS—and a different stock we find more appealing.

1. Underwhelming Long-Term Revenue Growth

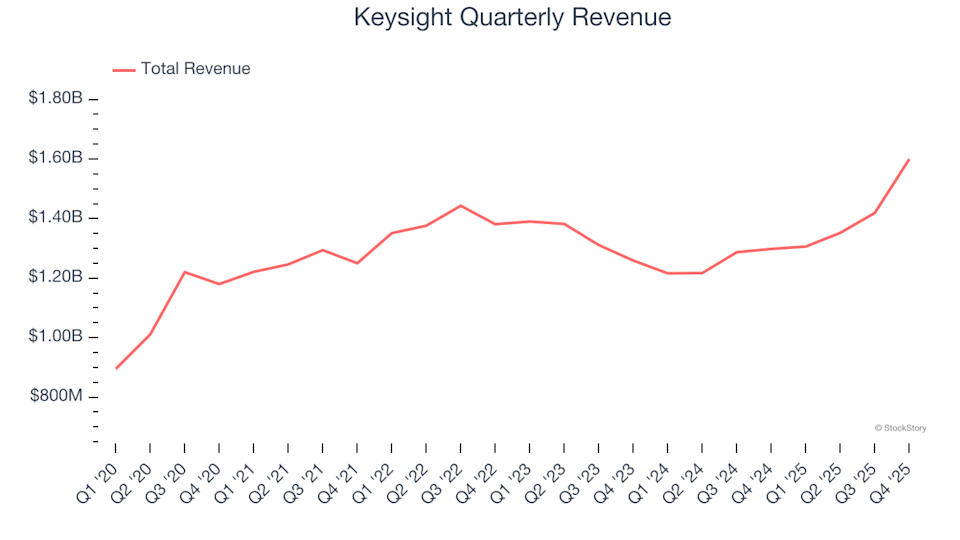

Examining a company’s revenue trajectory over several years can reveal its true caliber. While any business can post short-term gains, the best companies deliver consistent growth. Over the past five years, Keysight’s annualized revenue growth was just 5.7%, falling short of what we expect from leaders in the industrial sector.

Keysight Quarterly Revenue

2. Earnings Per Share Have Declined Recently

While long-term earnings trends are important, monitoring EPS over shorter periods can highlight emerging issues. Unfortunately, Keysight’s EPS has dropped by an average of 2.7% per year over the last two years, even as revenue increased by 3.1%. This indicates that profitability per share has slipped as the company has grown.

Keysight Trailing 12-Month EPS (Non-GAAP)

3. Diminishing Returns on New Investments

Return on invested capital (ROIC) measures how efficiently a company turns its capital into operating profit. While we favor companies with high returns, it’s the direction of ROIC that often surprises investors and impacts stock prices. Keysight’s ROIC has dropped significantly in recent years, suggesting that new investments are not delivering the returns they once did. While management has made smart moves in the past, the declining ROIC may point to a lack of lucrative growth opportunities going forward.

Keysight Trailing 12-Month Return On Invested Capital

Our Verdict

Keysight is not a poor business, but it doesn’t meet our standards for quality. After its recent rally, the stock is trading at a forward P/E of 32.9 (or $284.50 per share), which suggests that much optimism is already reflected in the price. There are likely better opportunities available. For example, consider one of our top picks in software and edge computing.

Top Stocks for Any Market Environment

Don’t Miss This: Our Top 6 Stock Picks for This Week. The market is quickly distinguishing between high-quality and overvalued stocks. With AI disrupting entire sectors at a rapid pace, you need more than just a list of solid companies to stay ahead.

Our AI-powered system identified Palantir before its 1,662% surge, AppLovin ahead of its 753% rise, and Nvidia before it soared 1,178%. Every week, it highlights six new stocks that meet our rigorous criteria.

Our recommendations have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Tecnoglass, which delivered a 1,754% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

3 Reasons to Steer Clear

Peru taps fuel reserves to combat worst energy crunch in two decades

3 Altcoins To Watch This Weekend | March 7 – 8