Here's Why You Should Add EAT Stock to Your Portfolio Right Now

Brinker International EAT continues to benefit from strong same-store sales momentum, marking its 19th consecutive quarter of comparable sales growth. Performance was driven by effective marketing and brand-building efforts that attracted guests, alongside improvements in food, service and restaurant atmosphere that encouraged repeat visits. Strong performance at Chili’s remains a key driver, supported by compelling value offerings, brand marketing and ongoing menu enhancements. Additionally, remodeling initiatives are enhancing the guest experience and supporting sustained engagement.

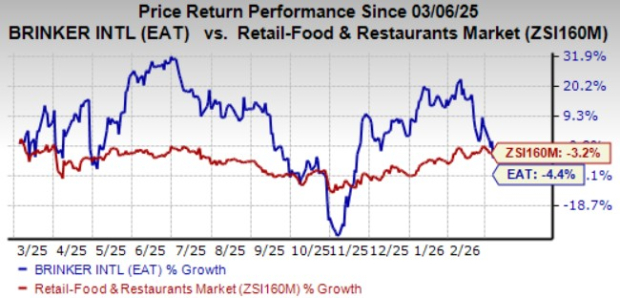

Shares of this casual dining chain have declined 4.4% in the past year compared with the Zacks Retail - Restaurants industry’s 3.2 fall. Its earnings topped the Zacks Consensus Estimate in each of the trailing four quarters, with an average surprise being 8.2%.

Image Source: Zacks Investment Research

The fiscal 2026 earnings estimate has edged up to $10.68 per share from $10.56 over the past 30 days. Although lingering inflation pressures and high costs are concerning, menu innovation and remodel activity have been driving growth.

Brinker International — a Zacks Rank #2 (Buy) stock — has a favorable VGM Score of A. Our research shows that stocks with a VGM Score of A or B, combined with a Zacks Rank #1 (Strong Buy) or 2, offer the best investment opportunities to investors.

Let’s delve deeper into the major driving factors.

Factors Aiding EAT Stock

Strong Same-Store Sales Growth: Brinker International delivered exceptional same-store sales growth during the second quarter of fiscal 2026, marking its 19th consecutive quarter of positive gains and outperforming the casual dining industry by a significant 680 basis points. This performance was spearheaded by Chili’s, which reported an 8.6% increase in comparable restaurant sales. This growth was fundamentally healthy, fueled by a robust 2.7% increase in guest traffic, strategic 4.4% price adjustments and a 1.5% positive mix shift.

The brand’s sustained momentum has resulted in an impressive 43% two-year cumulative comparable sales growth, driven by impactful marketing and core menu upgrades. Enhancements such as a premium bacon upgrade boosted burger sales and helped attract new guests while increasing visit frequency, supporting consistent top-line growth in a competitive restaurant environment.

Focus on Menu Innovation: Brinker International is driving traffic and brand relevance through targeted menu innovation focused on core offerings. In the second quarter of fiscal 2026, Chili’s upgraded key items, including thicker bacon strips and an enhanced Bacon Cheeseburger with triple the bacon, which generated about 43% higher sales than the prior version. The return of fan favorites like Skillet Queso also delivered strong sales growth.

The company continues to employ a “barbell” pricing strategy, anchored by the $10.99 “3 For Me” value platform while introducing premium items such as a new super-premium chicken sandwich lineup to support margins and check growth. At Maggiano’s, the brand has refocused on culinary fundamentals by bringing back classic dishes such as Gigi’s Butter Cake, Eggplant Parmesan, Baked Ziti and the traditional Meat Sauce, while increasing pasta portion sizes by 20% to enhance value perception.

Strong Chili’s Brand Momentum: Brinker International continues to benefit from strong momentum at Chili’s, which remains the primary driver of the company’s performance. The brand’s growth is supported by effective marketing campaigns, a compelling everyday value platform and improvements in food quality and service execution. In the fiscal second quarter, Chili’s same-store sales increased 8.6%, outperforming the casual dining industry by roughly 680 basis points. The brand’s bold signature flavors, generous portions and attractive entry-level pricing within its three-tier value lineup continue to resonate with guests and drive traffic.

The company also plans to significantly expand advertising efforts to leverage this sharp price positioning and further boost awareness and visits. Encouraged by the brand’s trajectory, management raised its full-year outlook and plans to add additional “sales layers” through premium menu innovation and investments in technology to ensure long-term relevance and consistent execution.

Higher ROE: Brinker International’s trailing 12-month return on equity (ROE) is indicative of its growth potential. The company’s ROE of 134.9% compares favorably with the industry’s 22.9%, which signals more efficiency in using shareholders’ funds than peers.

Other Key Picks

Some other top-ranked stocks from the Zacks Retail-Wholesale sector are:

Expedia Group, Inc. EXPE flaunts a Zacks Rank of 1 at present. The company delivered a trailing four-quarter earnings surprise of 3%, on average. EXPE stock has gained 15.8% in the past six months. The Zacks Consensus Estimate for Expedia Group’s 2026 sales and EPS indicates growth of 7.3% and 20.7%, respectively, from the prior-year levels.

Five Below, Inc. FIVE presently sports a Zacks Rank #1. The company delivered a trailing four-quarter earnings surprise of 62.1%, on average. Five Below's stock has rallied 46.5% in the past six months.

The Zacks Consensus Estimate for Five Below’s 2026 sales and EPS indicates growth of 22.1% and 25%, respectively, from the year-ago period’s levels.

Yum China Holdings, Inc. YUMC carries a Zacks Rank #2 at present. The company delivered a trailing four-quarter earnings surprise of 3.7%, on average. YUMC stock has climbed 17.9% in the past six months.

The Zacks Consensus Estimate for Yum China's 2026 sales and EPS indicates growth of 7.7% and 15.9%, respectively, from the year-ago period’s levels.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Cloudflare Gains 1.5% But Volume Dips to 247th in $550M as Earnings Loom

Kimberly-Clark Slips 0.31% in Quiet Trading; $520M Turnover Places at 259th

BC-Nikkei 225 Futures