HTH Rises 16.9% Over the Past Year: Is This the Right Time to Invest?

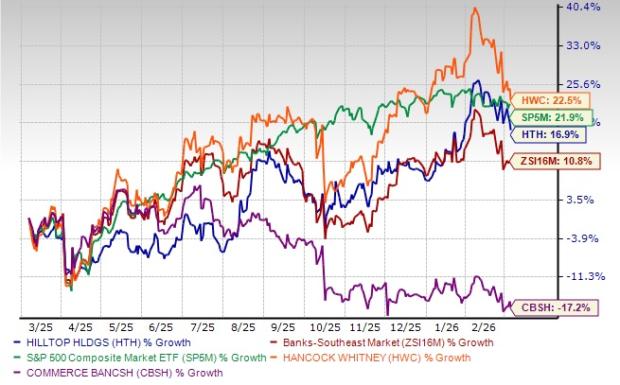

Hilltop Holdings Stock Performance Overview

Over the past year, shares of Hilltop Holdings Inc. (HTH) have climbed 16.9%, surpassing the 10.8% gain seen in the Southeast banking sector. However, this performance trails behind the broader S&P 500 Index, which advanced 21.9% during the same timeframe.

When compared to its industry peers, Commerce Bancshares, Inc. (CBSH) and Hancock Whitney Corporation (HWC), Hilltop Holdings' stock delivered mixed results. While HTH lagged behind Hancock Whitney, which saw a 22.5% increase, it outperformed Commerce Bancshares, whose shares dropped 17.2% over the year.

1-Year Stock Price Comparison

Source: Zacks Investment Research

Given this recent momentum, investors may wonder whether Hilltop Holdings has further room to grow. To answer this, it’s important to examine the company’s core financials and future outlook.

Key Drivers Behind Hilltop Holdings’ Growth

- Expansion in Net Interest Income (NII): Hilltop Holdings has prioritized boosting its net interest income. Although NII dipped in 2020, 2021, and 2024, it rebounded in 2022, 2023, and 2025, supported by acquisitions, healthy loan demand, and elevated interest rates. The net interest margin (NIM) also improved, rising from 2.81% in 2024 to 2.98% in 2025. Despite anticipated Federal Reserve rate cuts in 2025, management expects NII and NIM to remain resilient, thanks to steady loan demand and more stable funding costs. Projections suggest NII will maintain a compound annual growth rate (CAGR) of 5.3% through 2028, fueled by robust loan growth.

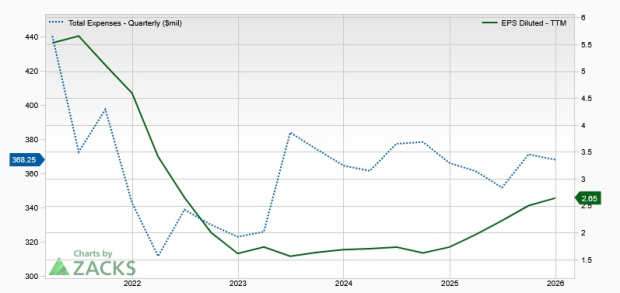

- Effective Cost Management: The company has demonstrated discipline in controlling expenses, with non-interest costs declining at a CAGR of 2.3% from 2019 to 2025. This reduction is largely due to strategic cuts in less profitable segments, such as Prime Lending.

Expense Reduction Trend

Source: Zacks Investment Research

- Strong Financial Position: As of December 31, 2025, Hilltop Holdings reported $825.5 million in debt and $1.23 billion in cash and bank balances. The company holds investment-grade credit ratings (BBB+/Baa2) with a stable outlook from both Fitch and Moody’s, ensuring favorable access to capital markets. Its solid liquidity and earnings enable ongoing shareholder returns, including regular dividend increases since 2016 and a new $125 million share repurchase program authorized through January 2027.

Challenges Facing Hilltop Holdings

- Asset Quality Concerns: Although provisions for credit losses dropped in 2024, they surged in 2022, 2023, and 2025. Net charge-offs have grown at a 20.4% CAGR over the past six years. With a challenging economic environment and rising delinquencies, both provisions and net charge-offs are expected to remain high in the near term, weighing on profitability. Provisions are projected to rise in 2026, and net charge-offs are forecasted to increase by 11.6% in 2027 and 28.7% in 2028.

- Underperformance in Mortgage Origination: The Mortgage Origination division continues to face headwinds. While origination volumes increased modestly in 2024 and 2025, they fell sharply in 2022 and 2023. To address these challenges, PrimeLending has reduced staff, consolidated branches, and adjusted fixed costs. Nevertheless, high mortgage rates, limited housing inventory, and affordability issues are likely to keep origination volumes under pressure, impacting segment performance.

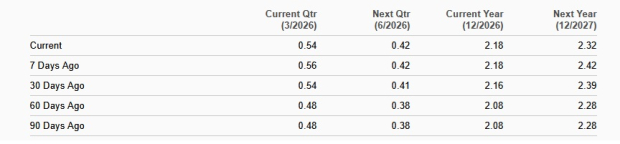

Reviewing Earnings Outlook and Valuation

Consensus estimates from Zacks place Hilltop Holdings’ 2026 earnings at $2.18 per share, a 17.4% decrease year-over-year. For 2027, earnings are expected to rise to $2.32 per share, a 6.3% increase. Over the past month, the 2026 estimate has been revised upward, while the 2027 forecast has been adjusted downward.

Earnings Estimate Trends

Source: Zacks Investment Research

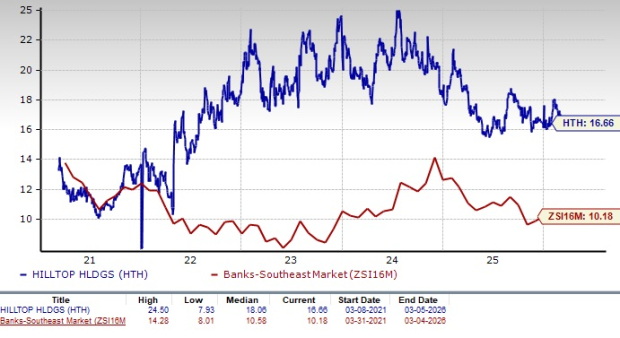

Hilltop Holdings currently trades at a forward price-to-earnings (P/E) ratio of 16.66, which is higher than the industry average of 10.18. This suggests the stock is valued at a premium compared to its sector peers.

Forward P/E Ratio Comparison

Source: Zacks Investment Research

For reference, Commerce Bancshares has a forward P/E of 12.58, while Hancock Whitney’s is 10.43, making HTH the more expensive option among these companies.

Investment Considerations for HTH

Hilltop Holdings’ prudent expense controls and strong balance sheet are likely to remain supportive of growth. Stable funding costs and ongoing loan demand should continue to benefit net interest income and margins, even as rates fall. However, persistent asset quality issues and weak mortgage origination volumes present significant challenges. Additionally, analysts remain cautious about the company’s earnings growth, and the elevated valuation adds to the uncertainty.

As a result, Hilltop Holdings may be best approached with caution by new investors. Those who already own shares might consider holding, as the company’s long-term prospects remain relatively steady.

Currently, Hilltop Holdings is rated as a Zacks Rank #3 (Hold).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

The $200 Billion Dilemma: Has the Time Come for Amazon to Issue a Dividend?

XOM | Oil Is About To Make a Move | LONG

$15.9B Unrealized Loss Hits BitMine and Strategy

Community banks and crypto industry ‘are allies’ in CLARITY Act debate: Exec