3 Factors to Consider for Selling COMP and One Alternative Stock Worth Purchasing

Compass Stock Performance Since September 2025

Since September 2025, Compass shares have remained relatively stagnant, experiencing a minor decline of 1.6% and hovering near $9.40. During this same timeframe, the S&P 500 saw a rise of 5.6%, highlighting Compass's underperformance compared to the broader market.

Should investors consider purchasing Compass now, or is it wise to exercise caution before adding it to your portfolio?

Reasons Compass May Not Outperform

We are currently opting to stay on the sidelines regarding Compass. Below are three factors that warrant caution, along with a stock we prefer over COMP.

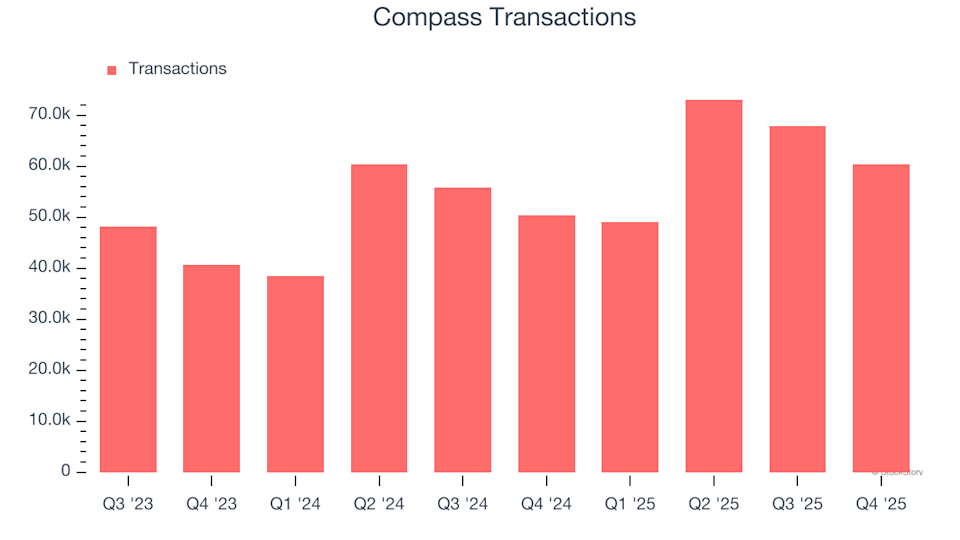

1. Sluggish Transaction Growth Signals Weak Demand

Revenue expansion for companies like Compass depends on both pricing and transaction volume, with transaction volume being particularly crucial since price increases have natural limits.

In the most recent quarter, Compass reported 60,328 transactions. Over the past two years, transaction growth averaged 21.7% annually, a figure that falls short of expectations. This lackluster performance may force Compass to reduce prices or invest in product enhancements to stimulate growth, potentially impacting short-term profitability.

Compass Transactions

2. Persistent Operating Losses Raise Concerns

Operating margin is a vital indicator of a company's profitability, representing net income before taxes and interest expenses, which are less tied to core business operations.

Although Compass's operating margin has improved over the past year, it still averaged -1.7% over the last two years. This negative margin stems from high operating costs and an inefficient expense structure.

Compass Trailing 12-Month Operating Margin (GAAP)

3. Lackluster Free Cash Flow Margin Restricts Growth Opportunities

At StockStory, we prioritize free cash flow because ultimately, cash is essential for covering expenses—accounting profits alone won't suffice.

Compared to its industry peers, Compass has demonstrated weak cash generation over the past two years, limiting its ability to reward shareholders. Its average free cash flow margin was just 2.5%, which is below expectations for a consumer discretionary company.

Compass Trailing 12-Month Free Cash Flow Margin

Our Verdict

We support businesses that serve everyday consumers, but with Compass, we remain observers rather than participants. The stock has lagged behind the market recently and trades at a forward P/E of 29.9 (or $9.40 per share). While this valuation isn't excessive, we don't see significant upside at present. There are more promising investment opportunities available. For example, consider a resilient company that owns the popular Taco Bell brand.

Top Stocks for Any Market Environment

ONE MORE THING: Discover the Top 6 Stocks for This Week. The current market is quickly distinguishing quality investments from overpriced ones. AI-driven shifts are impacting entire sectors without warning. In such a fast-moving environment, you need more than just a list of reputable companies.

Our AI platform identified Palantir before its 1,662% surge, AppLovin ahead of its 753% climb, and Nvidia prior to its 1,178% rally. Every week, it highlights six new stocks that meet rigorous criteria.

Past selections include well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Tecnoglass, which delivered a 1,754% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Analyst Breaks Down Theory On BlackRock’s XRP Play

Falling energy availability per person is the most significant challenge facing the world

Stevanato Group Caught in the Crossroads of Upward Trends and Downward Momentum

Best Meme Coins to Hold Long Term? 4 Cult Favorites With 500% Upside Potential This Month