3 Reasons to Consider Selling EXPI and One Alternative Stock Worth Buying

eXp World Shareholders Face Challenging Six Months

Investors in eXp World have endured a difficult half-year, with the company's share price tumbling by 41.3% to $6.50. This decline was largely influenced by weaker-than-expected quarterly performance, leaving many shareholders uncertain about their next steps.

Should you consider adding eXp World to your portfolio, or is it a potential risk?

Reasons We Expect eXp World to Lag Behind

Despite the stock's lower price, we are choosing to stay on the sidelines. Here are three main factors behind our decision to avoid EXPI, along with a stock we prefer instead.

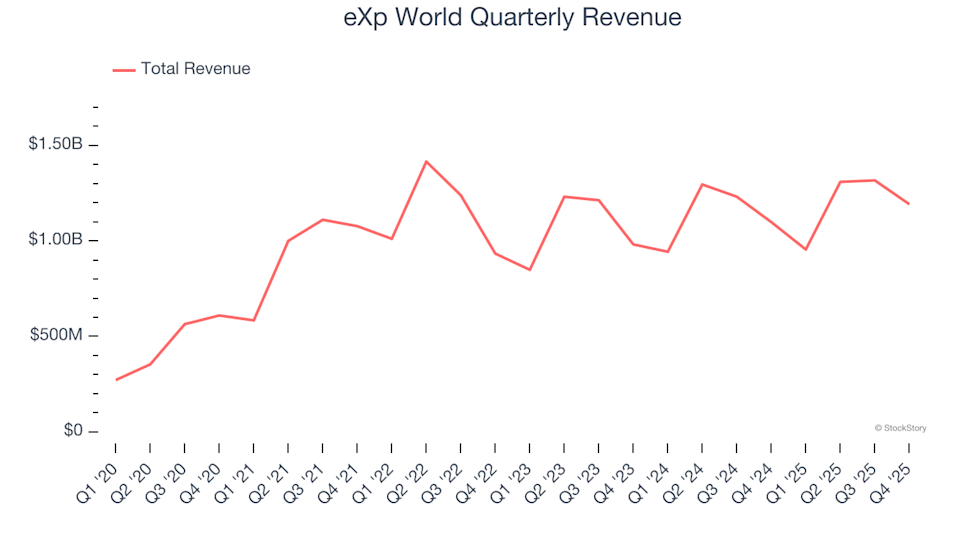

1. Revenue Growth Hasn't Met Expectations

Looking at a company's long-term track record can reveal its true quality. While any business might post strong numbers for a short period, only the best deliver consistent growth over time. Over the past five years, eXp World achieved a compounded annual sales growth rate of 21.6%. Although this is respectable, it doesn't quite reach the benchmark we set for consumer discretionary companies, a sector that typically benefits from strong industry trends.

eXp World Quarterly Revenue

2. Weak Free Cash Flow Margins Restrict Growth

At StockStory, we prioritize free cash flow because, ultimately, cash is what keeps a business running—accounting profits alone can't pay the bills.

Compared to its peers, eXp World has struggled to generate strong cash profits over the past two years. Its average free cash flow margin was just 3.1%, which is below what we typically look for in the consumer discretionary space. This limits the company's ability to reinvest or return value to shareholders.

eXp World Trailing 12-Month Free Cash Flow Margin

3. Declining ROIC Signals Ineffective Investments

Return on invested capital (ROIC) measures how efficiently a company turns its funding—both debt and equity—into operating profit.

We favor businesses that consistently deliver high returns, but the direction of ROIC is just as important. In recent years, eXp World has seen its ROIC drop significantly. Combined with already modest returns, this trend suggests the company has few lucrative growth opportunities left.

Our Verdict

While we appreciate companies that deliver value to consumers, we are not optimistic about eXp World at this time. Following the recent decline, the stock is trading at a forward P/E of 26.1 (or $6.50 per share), indicating that much optimism is already reflected in the price. We believe there are more attractive options available. Consider exploring one of our top picks in digital advertising instead.

Alternative Stocks to Consider

Don’t Miss: The Top 5 Momentum Stocks. The best time to invest in a standout company is when the market starts to recognize its potential. These businesses not only have strong fundamentals, but are also experiencing positive momentum right now—a powerful combination for investors.

Discover which stocks our AI platform is highlighting this week. Check out the latest Strong Momentum stocks—completely free.

Our selections have included well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Kadant, which delivered a 351% return over five years. Find your next potential winner with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

The Top Trending Crypto in 2026: BlockDAG’s 180x Launch Day Print Puts the 200x Mark Just Two Cents Out of Reach

Will Bitcoin follow oil’s historic surge and rally to $79K before the end of March?

Nubank (NU): Should You Buy, Sell, or Hold After Q3 Results?