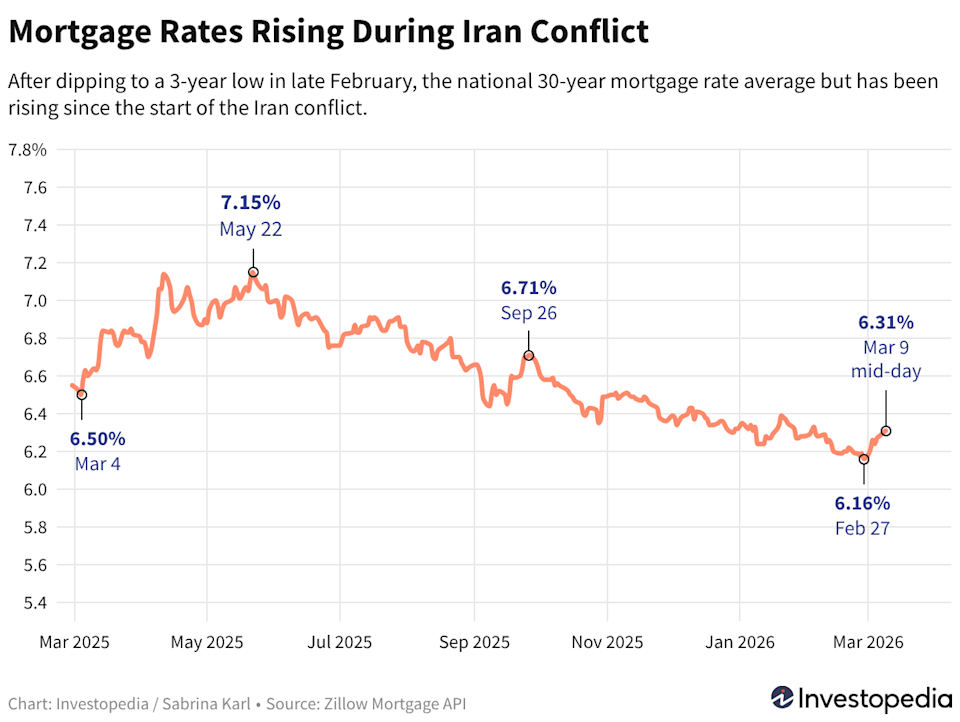

Mortgage rates dropped to their lowest point in three years—until tensions with Iran arose

Main Points

-

Mortgage rates dropped to an average of 5.98%—the lowest since 2022—but started to rise again as tensions in Iran escalated.

-

Investopedia’s daily average rate has increased by roughly 15 basis points over the past week, reflecting renewed market instability.

-

Although rates have edged up, they remain below last year’s peak, so being financially prepared is more important than trying to time the market perfectly.

Recently, mortgage rates provided some relief for buyers by dipping below 6% for the first time in over three years—a significant change after a prolonged period of high borrowing costs.

However, this improvement was short-lived. Once the conflict in Iran began, 30-year mortgage rates started to climb almost daily. While the increases have been moderate, they have disrupted the previous downward trend.

Current Mortgage Rate Trends

According to Freddie Mac’s weekly report, the average 30-year fixed mortgage rate fell to 5.98% on February 26—the first time it had dropped below 6% since September 2022. This figure includes loans with prepaid points. For loans without points, Investopedia’s daily 30-year rate average from Zillow showed a rate of 6.16%.

Just two days after this decline, conflict in the Middle East broke out. Following the February 27 drop to 6.16%, Investopedia’s daily average has steadily increased to 6.31%, a rise of 15 basis points in just a few days.

Why It’s Important

Mortgage rates can change rapidly in response to international events, making it difficult for buyers and those looking to refinance to predict the best time to act.

What’s Driving Rates Higher?

Mortgage rates are closely tied to global financial conditions. When uncertainty increases due to world events, investors often react quickly, which can impact borrowing costs.

After the Iran conflict began, financial markets became more volatile. Oil prices climbed, inflation worries returned, and long-term interest rates rose—pushing mortgage rates higher as well.

Even small shifts in investor sentiment can affect long-term rates, so mortgage costs can respond quickly to geopolitical changes. As long as uncertainty persists, rate fluctuations are likely to continue.

Advice for Homebuyers and Those Refinancing

Mortgage rates are shaped by a mix of factors, including inflation, bond market trends, and investor outlook—and they can move quickly when new economic or global developments arise. This makes predicting rates especially challenging.

Because of this, being financially prepared is often more important than waiting for the perfect rate. Buyers who are pre-approved and confident in their budget are better equipped to act quickly if they find the right home, rather than risk missing out while waiting for rates to drop further.

Even with the recent increases, today’s mortgage rates are still more favorable than they were a few months ago. However, even small changes in rates can significantly impact your monthly payments, so it’s crucial to focus on what fits comfortably within your budget.

For those considering refinancing, it’s important to carefully crunch the numbers. Homeowners with rates well above 6% might benefit from even a slight decrease, but factors like closing costs and how long you plan to stay in your home should be taken into account.

Your Initial Rate Isn’t Permanent

Locking in a mortgage rate now doesn’t mean you’re committed to it forever. If rates drop significantly in the future, refinancing could help you secure a lower payment—so you don’t have to miss out on a home you’re ready to buy today.

Read the original article on Investopedia.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

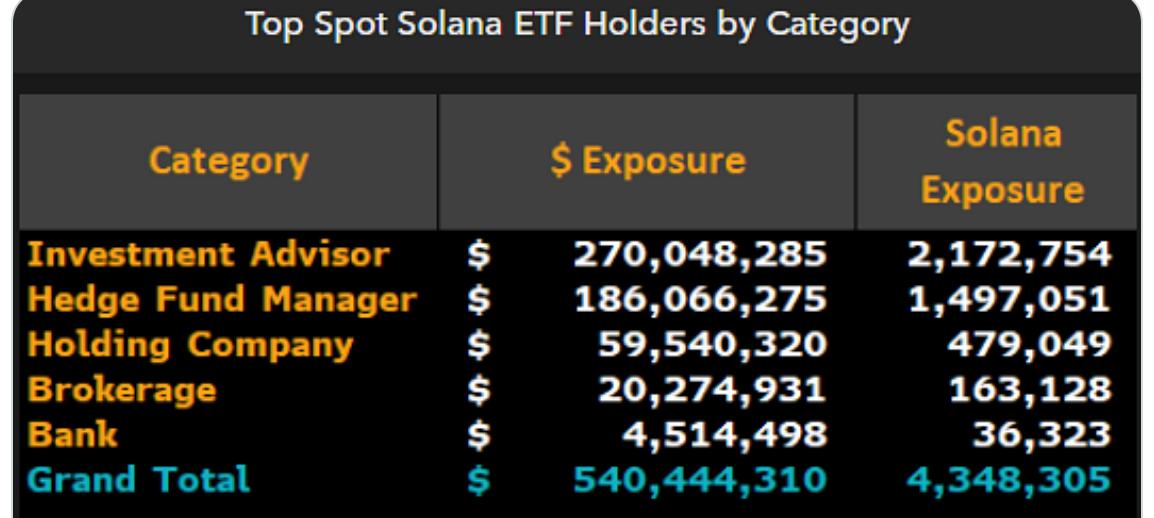

Wall Street funneled $540M into US Solana ETFs in Q4: Bloomberg

European freight truck makers brace for wave of low-cost Chinese rivals

IR (Infrared) 24-hour price fluctuation reaches 40.2%: trading volume slightly expands as support level is tested