JD.com Rises 1.63% Despite 412th-Ranked Volume Navigates Core Resilience and Logistics Growth Amid New Business Struggles

Market Snapshot

On March 9, 2026, JDJD+1.63%.com (JD) rose 1.63%, marking a modest gain despite a significant 43.5% decline in trading volume compared to the previous day. The stock’s volume of $0.35 billion ranked 412th in market activity, reflecting muted investor interest amid broader market dynamics. The performance contrasts with the company’s recent earnings report, which highlighted mixed financial results and strategic shifts in its core and new business segments.

Key Drivers

Core Business Resilience Amid Sector Challenges

JD.com’s Q4 2025 earnings underscored the resilience of its core retail operations, particularly in daily goods categories, which maintained double-digit growth. The 1P (first-party) business, however, faced headwinds, with electronics and home appliance revenue declining 11.99% year-over-year due to the high base effect from 2024 national subsidies. Meanwhile, the 3P (third-party) segment surged 20.13%, driven by 23.64% growth in logistics and service revenue. This divergence highlights the company’s ongoing transition toward platform monetization and third-party partnerships, which offset declines in its direct sales.

Logistics Expansion and Operational Efficiency

The logistics segment emerged as a key growth driver, achieving a 21.95% year-over-year revenue increase to RMB 63.53 billion. Despite a slight margin contraction to 2.97% from 3.50%, the division’s long-term strategic investments—such as plans to deploy 3 million robots, 1 million unmanned vehicles, and 100,000 drones—signal a focus on high-efficiency services. These advancements aim to strengthen JD’s logistics infrastructure, supporting both domestic operations and international expansion, particularly in Europe, where Joybuy’s trial operations have commenced in six countries.

Food Delivery and New Business Adjustments

New business losses narrowed by 5.94% quarter-over-quarter, with food delivery showing improved efficiency. While the segment reported a RMB 14.8 billion adjusted operating loss (an operating margin of -105.1%), reduced investment scale and optimized order structures contributed to progress. Synergies between food delivery and retail operations, including cross-category purchasing behavior and user growth, further bolstered integration. However, Jingxi and international ventures still dragged on profitability, underscoring the challenges of scaling non-core initiatives.

Forward-Looking Optimism and Valuation

Analysts project a recovery in JD’s profitability for 2026, contingent on continued food delivery efficiency gains and disciplined investments in overseas markets. Revenue is forecasted to reach RMB 1.4 trillion in 2026, with non-GAAP net profit expected to rise 30.56% year-over-year. A “Buy” rating and a target price of HKD 150.55 (12x 2026 PE) reflect confidence in the company’s ability to balance growth and margin stability. However, risks such as regulatory pressures, e-commerce margin compression, and geopolitical uncertainties remain critical headwinds.

Strategic Risks and Macroeconomic Pressures

The earnings report emphasized vulnerabilities in new business scalability, particularly if food delivery losses persist longer than anticipated. Additionally, overseas expansion—while promising—could strain resources if market share gains in Europe and other regions fall short. Macroeconomic factors, including weak retail sales growth and potential RMB depreciation, further complicate the outlook. These challenges highlight the need for JD to balance aggressive innovation with financial discipline, ensuring that investments in logistics and international markets align with long-term profitability goals.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Warsh plans meeting with Tillis while Senate confirmation stays stalled

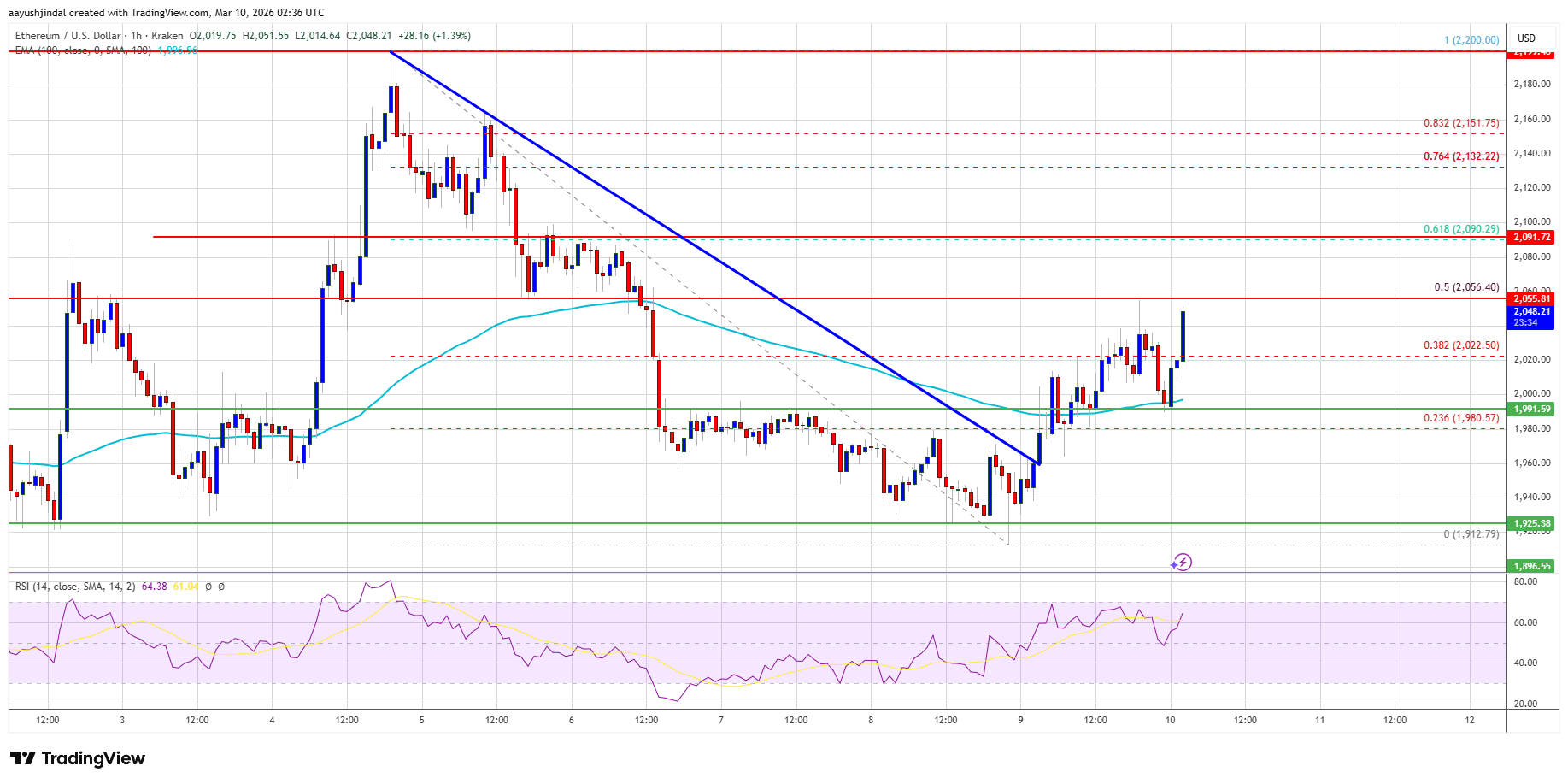

Ethereum Price Climbs Past $2,000, $2,200 Now in Bullish Crosshairs

ANIX Reports Smaller Losses but Revenue Remains at Zero

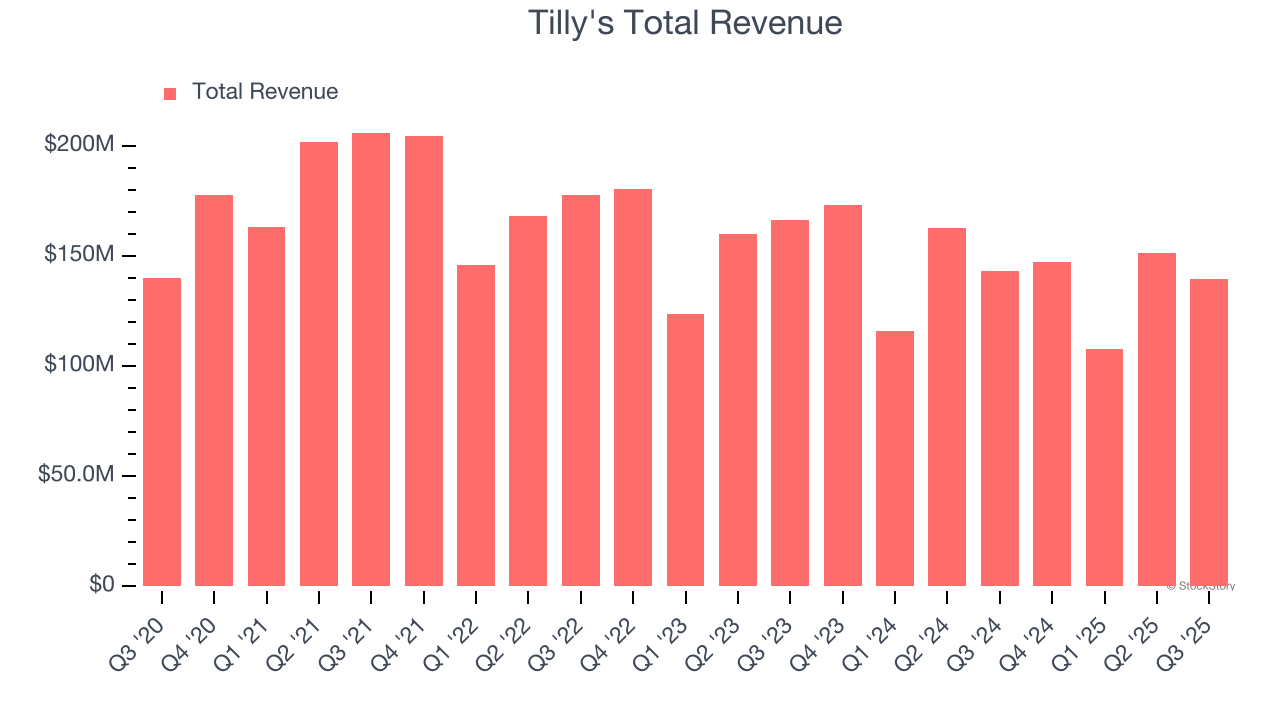

Tilly's (TLYS) To Report Earnings Tomorrow: Here Is What To Expect