OM Holdings Trading Strategy: Special Dividend and Strong Margins Indicate Potential for Revaluation

Key Catalyst and Market Reaction

The main trigger for recent market movement was a shareholder call held on March 9, following the announcement of the company's full-year 2025 results on February 27. Since the results were released, the stock has dropped approximately 3.4%, indicating that investors have not fully recognized the operational achievements outlined in the report. This muted response from the market presents a potential tactical opportunity.

Signals from the Shareholder Call

During the call, management revealed two important developments that may have been overlooked by the market:

- Special Dividend: On March 9, the company announced a special dividend of A$0.01 per share, providing a direct return to shareholders and signaling management’s confidence in near-term cash flows.

- Volume Growth: The company achieved a 6% increase in traded volumes for both ores and alloys during the fiscal year. This was a deliberate move to manage unit fixed costs amid weak pricing, demonstrating strong operational adaptability.

The market’s focus on declining revenue, rather than the company’s cost management and volume strategy, suggests a possible mispricing. The March 9 call reinforced the company’s commitment to operational discipline and capital returns, setting the stage for a potential revaluation if investors begin to appreciate these efforts.

Financial Overview: Margins and Balance Sheet Strength

Management emphasized that manganese alloy margins improved in FY2025, offsetting the impact of weak ferro-silicon prices. This improvement was driven by steady smelting output and increased volumes, which helped control fixed costs. As a result, the company’s most profitable segment remained resilient despite broader market challenges.

To support its operational strategy, the company completed a $168 million refinancing in the first quarter of 2025. This move bolstered the balance sheet, providing the liquidity necessary to pursue vertical integration and reducing short-term financial pressures.

Despite these positive developments, the stock traded at A$0.20 on March 9, below its recent peak of A$0.24. This discount appears to reflect ongoing concerns about oversupply in the ferro-silicon market, which has weighed on revenue. The key question is whether the market will eventually recognize the significance of margin improvements and the stronger balance sheet, potentially leading to a re-rating if supply concerns diminish.

Trading Strategy: Entry, Exit, and Upcoming Catalysts

This scenario presents a short-term trading opportunity, based on the expectation that the market will eventually acknowledge the company’s operational and financial strengths highlighted during the March 9 call. The stock is currently priced for continued revenue pressure, but management has demonstrated both margin resilience and improved financial stability. The next catalyst is the investor presentation scheduled for March 10, which could further reinforce the positive narrative.

The main opportunity lies in a potential rebound if manganese alloy margins remain strong and the special dividend is interpreted as a sign of ongoing capital returns. The recent 3.4% decline since the February results suggests that these positives are not yet fully reflected in the share price. A successful presentation could shift market sentiment and prompt a re-rating. However, if trade conditions and supply tightening do not improve, the company may continue to face price pressures despite its operational discipline.

For trade execution, consider entering below the current A$0.20 level, aiming for a rebound if the March 10 presentation confirms the margin and dividend story. Exit the position if there is a clear break above resistance or if negative news emerges regarding global supply dynamics. The March 10 investor presentation will be a critical event to monitor for the next move in the stock.

Technical Backtest: RSI Oversold Long-Only Strategy

- Entry Condition: Buy when RSI(14) falls below 30.

- Exit Conditions: Sell when RSI(14) exceeds 70, after 20 trading days, or if the position reaches a 10% gain (take-profit) or a 5% loss (stop-loss).

- Backtest Period: Last 2 years on OMHLF.

Backtest Performance Summary

- Total Return: 18.09%

- Annualized Return: 9.74%

- Maximum Drawdown: 12.52%

- Profit-Loss Ratio: 1.46

Trade Statistics

| Total Trades | 12 |

| Winning Trades | 6 |

| Losing Trades | 6 |

| Win Rate | 50% |

| Average Hold Days | 9.58 |

| Max Consecutive Losses | 3 |

| Profit-Loss Ratio | 1.46 |

| Average Win Return | 8.44% |

| Average Loss Return | 5.08% |

| Largest Single Gain | 15.06% |

| Largest Single Loss | 7.23% |

Conclusion

In summary, the company’s recent actions demonstrate strong operational and financial management, even as the market remains focused on revenue headwinds. The upcoming investor presentation is a key event that could prompt a reassessment of the stock’s value, especially if margin improvements and capital returns are emphasized. Traders should watch for confirmation of these themes as potential catalysts for a short-term rebound.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

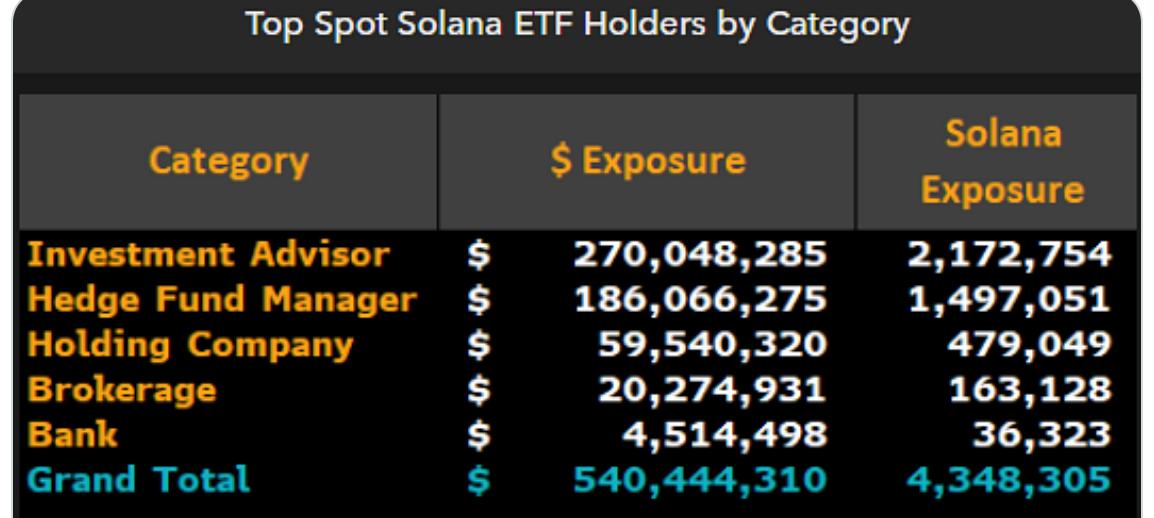

Wall Street funneled $540M into US Solana ETFs in Q4: Bloomberg

European freight truck makers brace for wave of low-cost Chinese rivals

IR (Infrared) 24-hour price fluctuation reaches 40.2%: trading volume slightly expands as support level is tested