EXCLUSIVE: Union Pacific CEO urges rail merger opponents to "stop dwelling on the past"

Union Pacific CEO Responds to Rail Merger Skepticism

Shakespeare once wrote, "what’s past is prologue," suggesting that history shapes the present and future. However, Union Pacific CEO Jim Vena believes this perspective doesn’t apply to the current transcontinental railroad merger.

During an exclusive conversation with FreightWaves, Vena addressed criticism surrounding Union Pacific’s proposed merger with Norfolk Southern. He firmly stated that this deal will not repeat the pricing and service challenges seen in previous transportation mergers, even as it transforms the American supply chain.

“It’s time to stop dwelling on the past and focus on what’s achievable,” Vena remarked from Union Pacific’s Omaha headquarters.

Union Pacific (UNP) has faced intense scrutiny from industry experts who question the financial logic behind the $85 billion agreement with Norfolk Southern (NSC).

Vena argued that focusing solely on the numbers is misguided. “Quality matters just as much. Our goal is to provide manufacturers and producers with a superior rail network, enabling them to compete globally,” he explained.

Merger Impact: Numbers and Efficiency

The merger aims to convert 1.4 million truckloads to intermodal transport within three years and shift 2 million truckloads to rail annually. The railroads claim the deal could reduce coast-to-coast railcar transit times by up to two days, making rail a viable competitor to trucking. Some industry insiders believe the time savings could be even greater. The unified route will also improve access to the Midwest, an area historically challenged by complex rail interchanges.

Questions about the merger intensified after the Surface Transportation Board (STB) rejected the initial application in December, citing incomplete information and requesting additional market data and agreement specifics.

Union Pacific and Norfolk Southern plan to submit a revised application in April.

Vena defended withholding certain competitive data, stating, “You have to protect sensitive information from rivals.” He reiterated that most future growth will come from capturing market share from trucking. However, some analysts criticized the railroads for counting dray-to-rail and rail-to-rail conversions as growth, rather than focusing solely on truck-to-rail shifts and new market opportunities.

Addressing Criticism and Regulatory Concerns

Vena is visibly frustrated by the negative feedback and questions some critics’ qualifications. “It’s easy to be pessimistic if you’re not responsible for delivering results,” he said, noting Union Pacific’s strong performance in efficiency, revenue, and safety. “Our team trusts the data we’ve compiled.”

The company also withheld Schedule 5.8, which outlines regulatory conditions that could allow Union Pacific to exit the deal. Vena explained, “Large transactions always include protections for both parties. If the STB required disclosure, we would comply. We requested confidentiality—it’s their decision. Revealing financial details to competitors is unreasonable.”

The STB recently proposed changes to reciprocal switching rules, potentially giving shippers more carrier options. Vena supports these changes, saying, “Reciprocal switching increases flexibility. I welcome the STB’s update.”

Service, Growth, and Modernization

When asked about Union Pacific’s recent slow growth, Vena emphasized that improved service can help the railroad meet the STB’s higher standards for mergers, which require not just maintaining but enhancing competition.

“We’re a robust, well-managed company,” Vena stated. “Currently, we handle a modest share of America’s daily freight tonnage. The merger will make freight movement more competitive, benefiting customers and the nation. Our aim is to offer more choices and shift freight from highways to rail.”

Vena highlighted that half of Union Pacific’s business is intermodal, and the merger will significantly expand this segment. The company continues to invest in new markets and facilities, including a steel plant in Phoenix and chemical plants in Louisiana, to provide customers with more options.

Union Pacific remains committed to upgrading its locomotive fleet by refurbishing older units instead of purchasing new ones. The company signed a $1.2 billion agreement with Wabtec in late 2025 to modernize its AC4400-series locomotives, marking the fourth such program since 2018 and bringing the total to 1,700 rebuilt engines.

“We’re investing heavily in modernization, rebuilding from the ground up for better efficiency and reliability,” said Vena, a former locomotive engineer. “If a superior product existed, we’d buy it, but our current strategy is effective.”

He also noted that Union Pacific has 1,500 surplus locomotives.

Industry Challenges and Customer Focus

Vena acknowledged that past transportation mergers, particularly among airlines and railroads, have not always benefited customers in terms of rates and choices. He pointed out that railroads have thrived despite being heavily regulated and requiring significant capital investment.

“Railroad costs over the past two decades have not kept pace with inflation,” he said. “Our customers are major corporations—Cargill, Exxon, ADM, Chevron, Walmart, Fedex, UPS—and they constantly push us to improve. We always ask how we can enhance our service. Operational efficiency, speed, and reducing touch points are key.”

Regarding service challenges, Vena explained that railroads must adapt to unpredictable customer demands. “Railroads can’t always operate with precision because customers’ needs vary daily. People should move away from focusing solely on operating ratios—that’s not our main driver.”

Activist Investors and Corporate Governance

Asked about Ancora, the activist investor responsible for leadership changes at Norfolk Southern and CSX (CSX), Vena commented, “Well-run companies that deliver for shareholders and customers are resilient against activist pressure. The American capitalist system ensures companies are held accountable for their performance.”

Regarding Norfolk Southern, Vena said, “Activists will always exist, but shareholders ultimately decide if management has the right strategy. The outcome of the Ancora campaign showed that the management team convinced shareholders of their vision.”

“There’s no better system,” he concluded.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

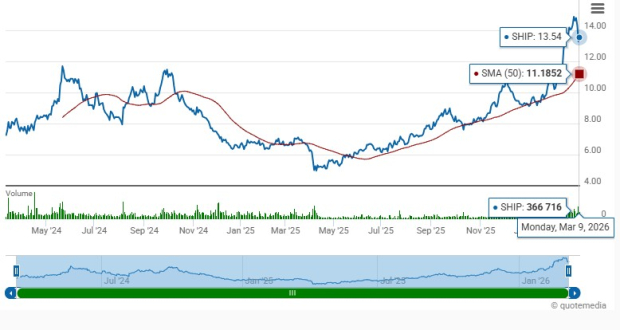

SHIP Jumps 95% Over the Past Year: Does It Remain a Top Stock Pick?

Exagen Inc. (XGN) Posts Fourth Quarter Loss, Surpasses Revenue Projections

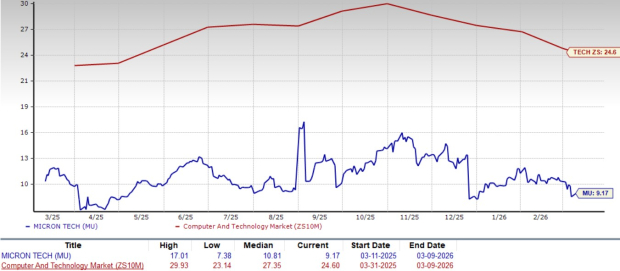

Micron Shares Surge 51% Over the Past Quarter: Can the Rally Continue?

USD: Conditional haven, limited durability – TD Securities