Micron Shares Surge 51% Over the Past Quarter: Can the Rally Continue?

Micron Technology: A Standout Performer in the Tech Sector

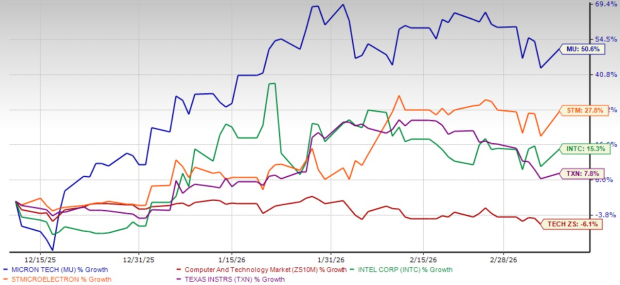

Micron Technology, Inc. (MU) has emerged as one of the top technology stocks, outperforming the broader market despite persistent economic and geopolitical headwinds. Over the past quarter, MU shares have surged by 50.6%, significantly outpacing the Zacks Computer and Technology sector, which saw a 6.1% decline during the same timeframe.

Micron's impressive rally has also eclipsed gains from other leading semiconductor companies such as STMicroelectronics (STM), Intel Corporation (INTC), and Texas Instruments, Inc. (TXN). In the last three months, STM advanced 27.8%, Intel rose 15.3%, and Texas Instruments increased by 7.8%—all trailing Micron’s performance.

Micron’s Recent Price Performance

Source: Zacks Investment Research

Capitalizing on the AI Revolution

Micron has benefited greatly from the surge in artificial intelligence, which has fueled demand for its memory products. With AI and high-performance computing continuing to drive the need for advanced memory solutions, Micron is well-positioned to take advantage of these trends, making it an appealing choice for investors seeking growth opportunities.

Micron’s Financial Strength

Despite facing global economic uncertainty, trade disputes, and geopolitical risks, Micron’s financial results remain robust. The company began fiscal 2026 with outstanding first-quarter results, showcasing its resilience.

- First-quarter revenue soared 57% year-over-year to $13.64 billion.

- Non-GAAP earnings per share (EPS) jumped 167% to $4.78.

- Both revenue and EPS exceeded Zacks Consensus Estimates by 7.26% and 22.25%, respectively.

- Non-GAAP gross margin improved to 56.8%, up from 39.5% a year earlier.

- Operating income (non-GAAP) rose to $6.42 billion from $2.39 billion, and operating margin expanded to 47% from 27.5%.

Micron’s Price, Consensus, and EPS Surprise

Looking ahead, analysts anticipate continued momentum for Micron in fiscal 2026. The Zacks Consensus Estimate projects revenue growth of 105.8% and EPS growth of 323.4% year-over-year. Notably, the EPS estimate for 2026 has been raised by $1.08 in the past week.

Micron’s Strategic Position in Emerging Technologies

Micron is at the forefront of several transformative technology trends, including artificial intelligence, high-performance data centers, autonomous driving, and industrial IoT. As AI adoption accelerates, demand for advanced memory like DRAM and NAND is climbing rapidly. Micron’s investments in next-generation DRAM and 3D NAND technologies ensure it remains competitive in meeting the needs of modern computing.

The company’s strategy to diversify beyond consumer electronics into more stable sectors such as automotive and enterprise IT has helped stabilize its revenue streams and reduce vulnerability to market cycles—a crucial advantage in the semiconductor industry.

Micron is also benefiting from strong demand for high-bandwidth memory (HBM). Its HBM3E products are gaining traction due to their energy efficiency and high bandwidth, making them ideal for AI applications.

In 2025, NVIDIA selected Micron as a key HBM supplier for its GeForce RTX 50 Blackwell GPUs, highlighting Micron’s integral role in the AI supply chain. The company’s advanced packaging facility for HBM in Singapore, set to open this year and expand further by 2027, demonstrates its commitment to scaling up for AI-driven markets.

Attractive Valuation Supports Investment Case

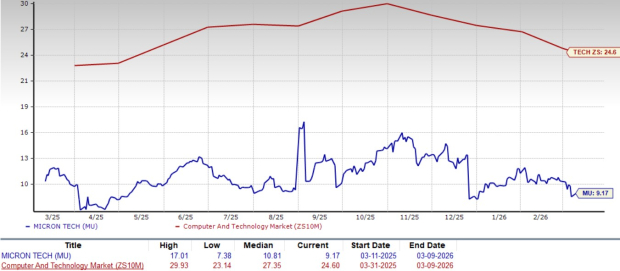

Despite its recent rally, Micron’s stock remains attractively valued. It currently trades at a forward 12-month price-to-earnings (P/E) ratio of 9.17, well below the sector average of 24.60. This discount enhances its appeal for long-term investors.

Micron’s Forward P/E Ratio

Source: Zacks Investment Research

Compared to its peers, Micron’s P/E ratio is lower than those of STMicroelectronics (26.08), Texas Instruments (29.22), and Intel (75.20). This relative valuation, combined with its exposure to AI growth, strengthens the case for investing in Micron.

Conclusion: Micron Remains a Strong Buy

Micron Technology stands out for its solid fundamentals, leadership in AI-driven memory solutions, and disciplined innovation. Trading at a discount compared to other major semiconductor firms, Micron offers compelling long-term growth prospects. Given these factors, accumulating shares of MU appears to be a wise move.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Pre-market activity is influenced by current spot oil prices

The Australian dollar reaches its highest point since 2023. Here are four factors driving its upward movement

Cresset Elevates Susie Cranston—Accomplished Wealth Creator—to CEO as Growth Drivers Converge

Teladoc’s Guidance Reset Caps Earnings Pop as Profit Path Stays Uncertain