Is Innodata's Hybrid AI Strategy Set to Boost Margins Ahead?

Innodata Inc. INOD is positioning itself at the center of the rapidly evolving artificial intelligence ecosystem, and its emerging hybrid AI model could play a critical role in expanding profitability. The company is increasingly combining human expertise with automation, synthetic data generation and proprietary evaluation platforms, creating what management describes as a hybrid human-technology approach to AI development. This shift has the potential to improve operating leverage while supporting strong revenue growth.

In 2025, Innodata delivered impressive financial momentum, with revenue rising 48% year over year to $251.7 million and fourth-quarter revenue reaching $72.4 million, up 22% year over year. The company also reported adjusted EBITDA of $57.9 million for the year, reflecting expanding demand for its AI data engineering capabilities.

The company’s hybrid model is built around data engineering and AI lifecycle services that support the development, evaluation and optimization of large language models and AI agents. Innodata increasingly works with clients not only to supply training data but also to diagnose model performance, design targeted datasets and validate improvements. This approach moves the conversation from simply providing data to delivering measurable improvements in model outcomes.

Management believes this model will become more margin accretive over time. As automation tools, evaluation platforms and synthetic data systems scale, they should reduce reliance on purely labor-intensive processes while improving efficiency. Over time, these hybrid solutions are expected to support gross margins above current targets as software-enabled workflows gain scale.

Innodata’s innovation pipeline—including agentic AI evaluation systems, adversarial testing frameworks and robotics data engineering—also opens new high-value use cases across enterprise AI and physical AI markets. If adoption continues to expand, the hybrid model could strengthen revenue quality and position the company for sustained margin expansion in the years ahead.

Competitors in the AI Data Engineering and Model Training Space

Two notable competitors operating in areas similar to Innodata’s AI data engineering and model-training ecosystem are C3.ai AI and Palantir Technologies PLTR. Both companies operate in adjacent parts of the AI value chain and increasingly focus on enterprise AI deployment, model optimization and data-driven platforms.

C3.ai develops enterprise AI software platforms that allow organizations to build, deploy and scale machine learning applications across industries such as energy, defense and manufacturing. While Innodata focuses on high-quality dataset creation and AI model optimization, C3.ai emphasizes application development and AI deployment at scale. Still, the company relies heavily on structured datasets and model training pipelines, placing it in a related competitive landscape. As generative AI adoption accelerates, C3.ai is expanding its enterprise AI offerings, positioning itself as a key player in operationalizing AI across large organizations.

Palantir is another important competitor operating in data-driven AI infrastructure. Its platforms—such as Foundry and AIP—help enterprises integrate data, train models and deploy AI systems across complex workflows. Palantir increasingly supports AI model development, evaluation and operational deployment, which overlaps with Innodata’s role in improving model performance through specialized datasets. With strong government and enterprise adoption, Palantir remains a major force in the AI ecosystem alongside companies like Innodata.

INOD’s Price Performance, Valuation & Estimates

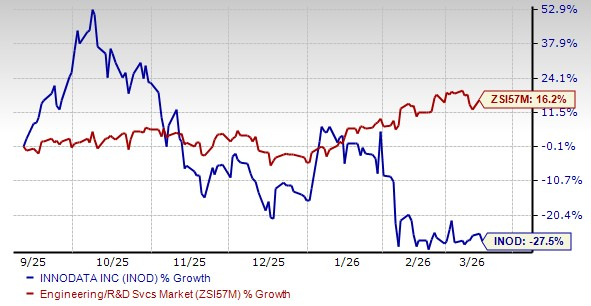

Shares of Innodata have lost 27.5% in the past six months, underperforming the Zacks Engineering - R and D Services industry’s 16.2% growth.

INOD’s 6-Month Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, INOD trades at a forward price-to-earnings ratio of 39.67, much higher than the industry’s average of 26.03.

P/E (F12M)

Image Source: Zacks Investment Research

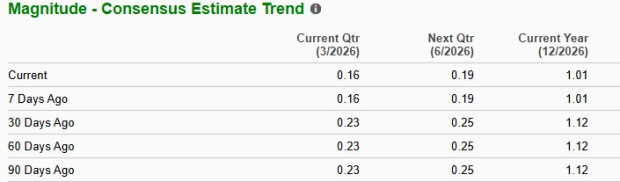

The Zacks Consensus Estimate for INOD’s 2026 earnings has declined to $1.01 from $1.12 per share in the past 30 days. The estimated figure indicates 9.8% growth from the 2025 level.

Image Source: Zacks Investment Research

INOD currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

King's College's Aluminum Innovation May Transform Rare-Earth Supply Chains

Ukraine’s Deep Strikes on Russia’s Industrial Base Test Market Bets on Defense Sector Resilience

Oil Drops 12% Amid Uncertainty Surrounding Hormuz Shipping Status

VTv Therapeutics: Fourth Quarter Earnings Overview