Agnico Eagle: Surge in Gold Prices Fuels Shares—Does Exploration Play a Key Role in This High-Risk Commodity Wager?

Gold Price Surge Takes Center Stage

Currently, the spotlight in financial markets is firmly on the dramatic rise in gold prices, which is the primary force propelling Agnico Eagle’s stock upward. Investors and market watchers are overwhelmingly focused on gold’s reputation as a safe-haven asset, rather than on company-specific exploration activities or drilling updates. This overarching trend is dominating headlines and shaping sentiment.

In 2026, gold has climbed 18%, with the precious metal approaching $5,140 per ounce. Ongoing geopolitical instability is a key factor fueling this rally, and expectations are that these conditions will continue to support elevated prices. For gold producers like Agnico Eagle, this price environment is the main growth engine. The company’s shares have risen 2.78% today, closely tracking the surge in gold itself.

This is not a fleeting spike, but rather a fundamental shift. The sector is grappling with limited new discoveries and aging mines, leading to persistent supply constraints and a long-term imbalance that supports higher prices. Meanwhile, investor appetite remains strong, as evidenced by robust ETF inflows. For Agnico Eagle, rising gold prices directly boost revenue and profitability, as demonstrated by a sharp increase in adjusted net income in the latest quarter. In this narrative, the gold rally is the protagonist, with Agnico Eagle’s stock as its most direct beneficiary.

The Role of Exploration: Important, But Not the Main Focus

Although Agnico Eagle’s exploration division delivered solid results last year, these achievements have not captured the market’s attention in the same way as the gold rally. The company’s 2025 exploration program resulted in a 2% increase in reserves, reaching 55.4 million ounces, reinforcing the company’s long-term production outlook. However, these operational milestones play a supporting role, made possible by the financial strength generated from high gold prices.

The real momentum comes from the surge in gold prices. Agnico Eagle’s impressive $4.4 billion in free cash flow in 2025 is a direct result of capitalizing on the gold rally. This influx of cash is what enables further exploration, not the other way around. In this scenario, exploration benefits from the gold price boom, rather than driving it. The company’s ability to turn higher gold prices into strong cash flow underpins ongoing drilling and project development.

This contrast is evident when comparing Agnico’s disciplined approach to the broader Australian exploration sector, which saw a 49.3% increase in exploration spending in 2025. For Agnico, investment is targeted and strategic, focusing on expanding existing mines and advancing key projects like Malartic and Detour Lake, rather than speculative ventures.

In summary, exploration is not the headline act in today’s market narrative. Investor interest and search trends are overwhelmingly centered on gold prices. While exploration results are vital for Agnico Eagle’s future, they play a supporting role in a story largely dictated by commodity markets. The company’s exploration efforts are funded by the profits generated from the ongoing gold rally.

Valuation and What’s Next: Riding the Gold Narrative

Agnico Eagle’s investment appeal now rests on its premium valuation and anticipation of the next major catalyst. The stock is trading at a forward P/E of 25.7, reflecting investor confidence in sustained high gold prices and the company’s operational strength. This valuation is not a bargain, but rather a wager on the continuation of the gold rally and Agnico’s ability to capitalize on it.

The upcoming earnings report, set for April 30, 2026, is the next significant event. This release will reveal whether Agnico Eagle can maintain its recent momentum, following a quarter of robust adjusted earnings and strong free cash flow driven by higher realized gold prices. Investors will be watching closely to see if the company can sustain its margins and continue converting gold price gains into healthy cash flow, which supports both exploration and shareholder returns.

However, this premium valuation comes with increased risk. The 12-month price target of $251.14 suggests further upside, but much of the positive outlook is already reflected in the current share price. Any downturn in gold prices, easing of geopolitical tensions, or setbacks on key projects could quickly alter the narrative. While Agnico Eagle’s focus on stable jurisdictions like Canada, Finland, and Mexico reduces political risk, it also means the company is less exposed to high-risk, high-reward frontier exploration. The main operational risk lies in the development of projects such as the Upper Beaver deposit, where progress is still being assessed.

In conclusion, Agnico Eagle’s fortunes are closely tied to the ongoing gold rally. The current valuation leaves little margin for error, making the stock sensitive to changes in the gold price narrative or any missteps in execution. The upcoming earnings announcement will be a crucial test for the company’s ability to deliver on high expectations.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

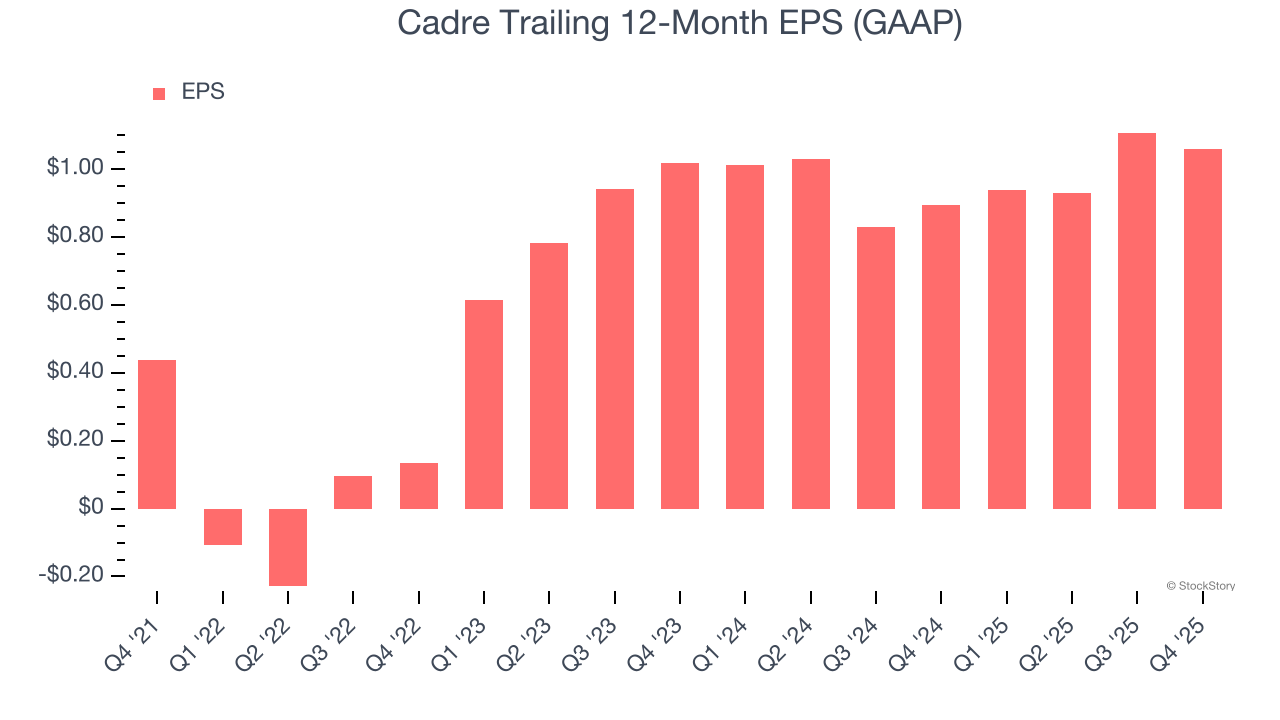

Cadre (NYSE:CDRE) Misses Q4 CY2025 Revenue Estimates

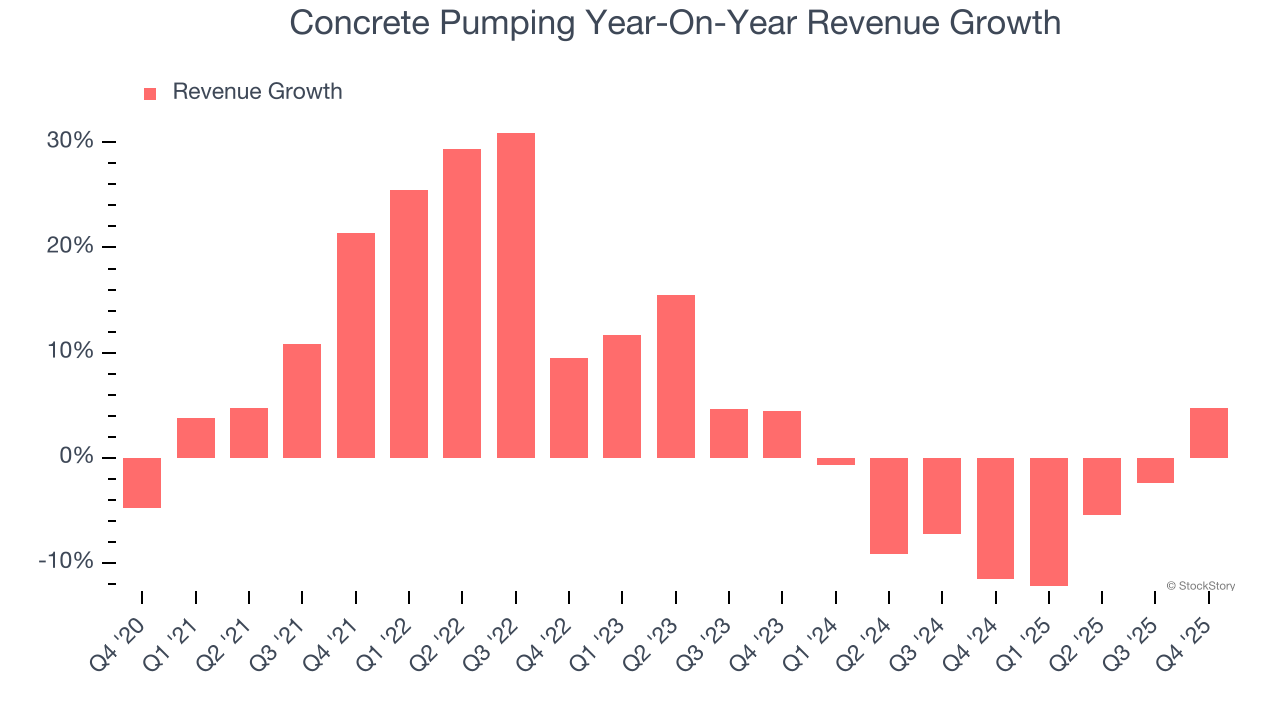

Concrete Pumping (NASDAQ:BBCP) Surprises With Strong Q4 CY2025

US recession chances climb as oil prices fluctuate