SHOP Drops 11% Over Half a Year: Should You Buy, Sell, or Hold This Stock?

Shopify Stock Lags Behind Sector and Industry Peers

Over the last half-year, Shopify (SHOP) shares have dropped by 10.8%, falling short of the Zacks Computer and Technology sector’s 3.4% gain and the Internet-Services industry’s impressive 37.9% rally. This underperformance highlights investor concerns about Shopify’s ability to maintain its growth momentum while continuing to invest heavily in new products, artificial intelligence-driven commerce solutions, and merchant-focused tools.

Compared to other major players like Amazon (AMZN), Wix.com (WIX), and Commerce.com (CMRC), Shopify’s stock has shown mixed results. During the same period, Amazon’s shares slipped 7.5%, Wix.com tumbled 47.3%, and Commerce.com declined 38.4%.

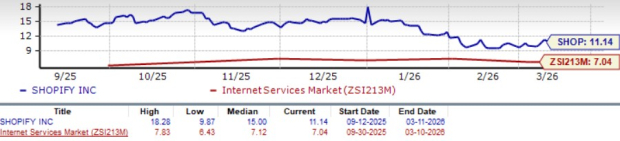

Recent Performance of Shopify Stock

Source: Zacks Investment Research

Valuation Concerns: Is Shopify Overpriced?

Shopify currently holds a Value Score of F from Zacks, indicating that the stock is considered overvalued. Its forward 12-month price-to-sales ratio stands at 11.14, significantly higher than the sector average of 6.18 and the industry average of 7.04. In comparison, Amazon, Wix.com, and Commerce.com trade at much lower price-to-sales multiples of 2.8, 2.25, and 0.68, respectively.

This premium valuation is difficult to justify, especially as Shopify faces ongoing pressure on gross margins due to a shift toward lower-margin Merchant Solutions revenue and the rapid growth of Shopify Payments. Notably, transaction and loan losses are projected to nearly double from $227 million in 2024 to $417 million in 2025. Broader economic challenges, such as tariff uncertainties and weaker consumer spending, add to these headwinds.

Forward Price/Sales Ratio Comparison

Source: Zacks Investment Research

Stable Earnings Outlook for 2026

Analyst consensus for Shopify’s first quarter 2026 earnings remains at $0.32 per share, unchanged over the past month and representing a 28% increase year-over-year. Revenue for the quarter is expected to reach $3.08 billion, up 30.55% from the previous year.

For the full year 2026, consensus estimates project earnings of $1.76 per share, a 50.43% increase from the prior year, with revenues anticipated at $14.51 billion, reflecting 25.6% growth.

Shopify’s Price and Consensus Trends

Shopify’s Strategic Focus on AI-Driven Commerce

Shopify is doubling down on artificial intelligence to drive the next wave of digital commerce. The company has partnered with Google to create the Universal Commerce Protocol, an open standard that enables AI agents to interact with merchants across leading platforms, including ChatGPT and Microsoft Copilot. Its Agentic Storefronts solution allows merchants to easily distribute product catalogs to major AI-powered channels.

Shop Campaigns, Shopify’s performance marketing tool, saw its revenue double and merchant adoption triple in 2025, signaling strong demand for AI-powered customer acquisition. These efforts have fueled a 35% year-over-year increase in Merchant Solutions revenue in the fourth quarter of 2025, reaching $2.9 billion.

Shopify is also building the infrastructure needed for large-scale AI shopping experiences, with orders from AI search channels rising sharply over the past year. While these initiatives could enhance Shopify’s relevance and support long-term gross merchandise volume growth, competition is intensifying as other companies ramp up their own AI commerce offerings. The ability to monetize these early-stage projects remains to be seen.

International Growth Accelerates

Expanding globally remains a major growth driver for Shopify. The company has broadened its platform with more localized payment methods, language support, and cross-border commerce tools. Shopify Payments is now available in 60 countries, Shopify Capital in eight, and Managed Markets 2.0 offers faster international payouts and more payment options. These enhancements help merchants sell worldwide while managing compliance, payments, and logistics within Shopify’s ecosystem.

International revenue climbed 36% in 2025, outpacing overall company growth of 30%. Nearly half of Shopify’s merchants are now based outside North America. Growth has been balanced between attracting new merchants and deepening engagement with existing ones. However, currency fluctuations and diverse regulatory environments could slow expansion in the near term.

Final Thoughts

Shopify faces a rich valuation and near-term challenges from margin pressures and rising transaction and loan losses. Nonetheless, the company’s expanding AI initiatives and international reach provide a positive outlook for long-term growth. Current shareholders may want to hold their positions, given Shopify’s resilient growth and broad merchant adoption.

Shopify currently holds a Zacks Rank #3 (Hold), suggesting that prospective investors may want to wait for a more attractive entry point.

Spotlight: Top Semiconductor Stock Pick

A lesser-known company in the semiconductor space is poised to benefit from the next wave of industry growth, occupying a niche not served by giants like NVIDIA. With robust earnings and a growing customer base, this company is well-positioned to capitalize on surging demand for artificial intelligence, machine learning, and the Internet of Things. The global semiconductor market is expected to soar from $452 billion in 2021 to $971 billion by 2028.

Additional Resources

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

The Hanover's Stock is Priced at 1.73 Times Its Book Value: Does This Justify the Valuation?

Swiss Franc continues to face downward pressure even amid ongoing geopolitical uncertainties

XRP Surges Toward $1.43 After Rebounding From $1.33 Demand Zone — Is $1.50 the Next Test?

How the US Strategic Petroleum Reserve functions and the reasons behind its current use