Fifth Third Shares Surge 2.7% on $560M Volume Boost as Merger and Earnings Drive Rank 217 Trading Activity

Market Snapshot

Fifth Third Bancorp (FITB) shares rose 2.71% on February 25, 2026, closing at $51.56, as the stock saw a significant surge in trading activity. The company’s stock volume reached $560 million, a 32.24% increase compared to the previous day, ranking it 217th in trading activity on the day. This performance followed a broader market rally, with the S&P 500 up 0.81%. The rise in volume and price suggests heightened investor interest, potentially driven by recent corporate developments and earnings momentum.

Key Drivers

Earnings Outperformance and Revenue Growth

Fifth Third reported Q4 2025 earnings of $1.04 per share, exceeding the $1.00 forecast by 4%, while revenue hit $2.34 billion, matching expectations. The bank’s adjusted revenues grew 5% year-over-year, reflecting stronger loan growth and effective cost management. These results, combined with a 7.53% stock price surge in the prior quarter, indicate robust operational performance. Analysts highlighted the bank’s ability to maintain profitability amid a challenging interest rate environment, which likely contributed to the recent price appreciation.

Strategic Merger and Synergy Potential

The bank’s pending $850 million in expense synergies from its Comerica merger, expected to finalize on February 1st, is a critical catalyst. The deal is designed to strengthen Fifth Third’s market position by expanding its presence in key commercial banking and wealth management segments. Despite the post-earnings pre-market dip of 0.12%, the merger’s long-term benefits—such as enhanced scale and cost efficiency—remain a focal point for investors. The integration phase, however, has introduced short-term volatility, as markets weigh execution risks against anticipated gains.

2026 Financial Targets and Guidance

Fifth Third has set ambitious 2026 goals, including a 19% return on tangible common equity, net interest income of $8.6–8.8 billion, and mid-single-digit loan growth. These targets, coupled with a strong balance sheet and 51 consecutive years of dividend payments (currently yielding 3.25%), underscore the bank’s commitment to shareholder value. The 3.25% yield, above the sector average, further appeals to income-focused investors, supporting the stock’s resilience.

Mixed Investor Sentiment and Market Cautiousness

While the earnings beat and strategic initiatives are positives, investor sentiment remains cautiously balanced. The pre-market price decline following the earnings report suggests some skepticism about the merger’s integration challenges and broader macroeconomic risks. Additionally, the bank’s forward P/E ratio of 11.05, lower than its 5-year average of 14.61, indicates undervaluation relative to future earnings potential. Analysts have maintained a “In-Line” rating, with price targets ranging from $49 to $61, reflecting confidence in long-term fundamentals despite near-term uncertainties.

Dividend Stability and Long-Term Appeal

Fifth Third’s uninterrupted dividend streak since 1975, now at 51 years, reinforces its reputation for financial stability. The 3.25% yield, combined with a strong return on equity (12.19% trailing), positions the stock as a defensive play in a market wary of rate hikes. While the bank’s recent performance (up 10.15% year-to-date) outperforms the S&P 500’s 1.47% gain, its 5-year return of 75.82% lags behind the 81.39% benchmark. This disparity highlights the need for sustained earnings growth to close the gap with broader market averages.

Conclusion

Fifth Third’s stock rally is underpinned by strong earnings, strategic mergers, and long-term financial discipline. However, the path to its 2026 targets depends on successful merger integration and macroeconomic resilience. With a balanced mix of growth initiatives and defensive attributes, the bank remains a key player in the regional banking sector, though investors are advised to monitor execution risks and broader interest rate trends.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

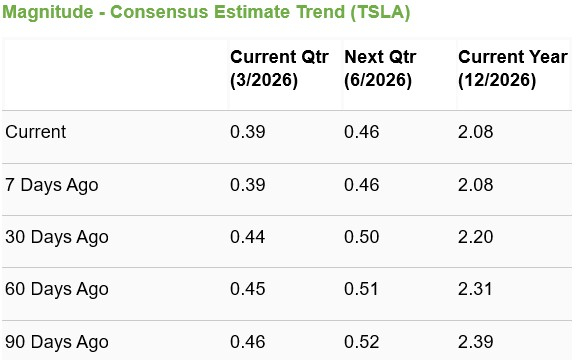

Tesla’s Challenges in Europe Persist: Is It Wise to Rely on Their Autonomy Commitments?

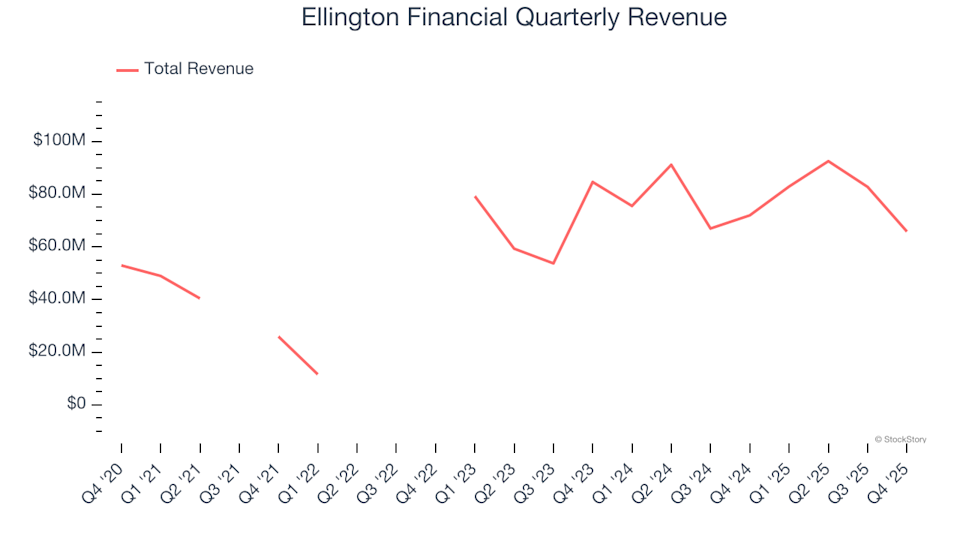

Ellington Financial (NYSE:EFC) Falls Short of Q4 CY2025 Revenue Projections

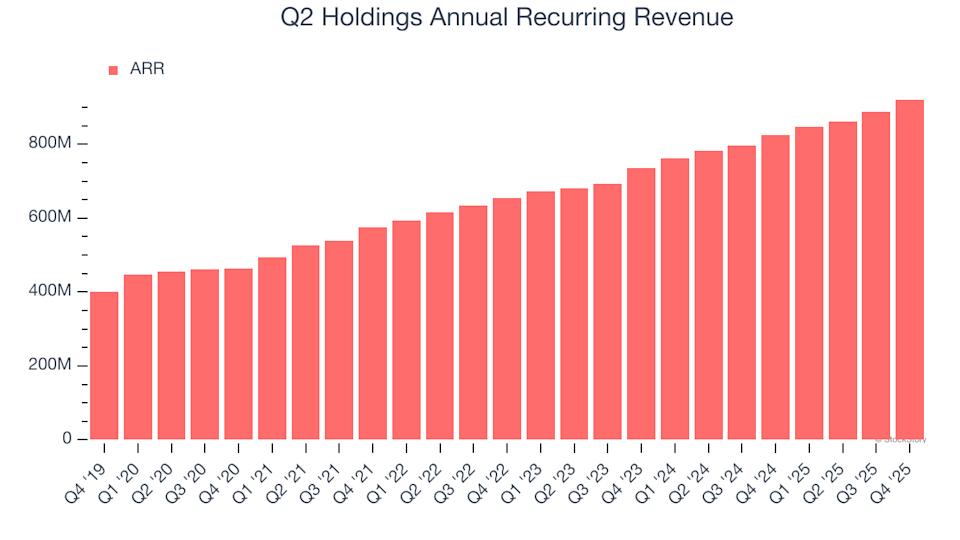

3 Reasons to Steer Clear of QTWO and One Alternative Stock Worth Buying

Morning Minute: Circle's Financial Results Mark a Landmark Day for the Crypto Industry