Why Home Depot Anticipates Better Comparable Sales in the Latter Half Compared to the Earlier Half

Home Depot’s Outlook for Fiscal 2026: Stronger Growth Expected in Second Half

Home Depot, Inc. (HD) anticipates that its comparable sales will show more robust growth during the latter half of fiscal 2026 compared to the first half. The company projects that same-store sales for the year will range from flat to a 2% increase. This forecast is primarily influenced by the easing of major challenges that weighed on results in the second half of fiscal 2025.

During the most recent earnings call, leadership explained that the anticipated improvement in the back half of the year is largely due to the impact of storm activity in fiscal 2025. Severe weather often drives temporary surges in demand for products like roofing, building supplies, and repair materials. When such events do not repeat in the following year, it can lead to uneven year-over-year comparisons across quarters.

The first half of fiscal 2026 is expected to face tougher comparisons because of last year’s weather-driven sales spikes. As the year progresses and the company moves past these periods, the comparison base becomes easier, which should support stronger same-store sales in the second half.

Despite ongoing challenges such as high mortgage rates and affordability issues in the housing market, Home Depot reports that underlying demand has remained steady. By the latter part of fiscal 2026, the company expects its significant investments in professional customer services to deliver more meaningful results. Additionally, continued growth and integration of SRS and GMS are set to further enhance performance.

These strategic efforts, combined with more favorable year-over-year comparisons later in the year, reinforce management’s confidence in accelerating sales momentum as fiscal 2026 unfolds.

Recent Performance and Competitive Landscape

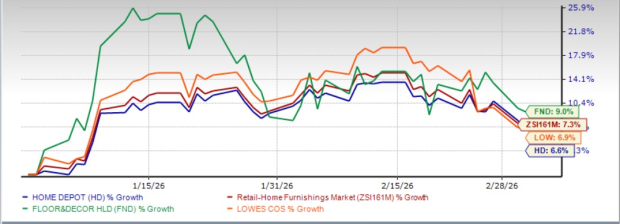

Home Depot, competing with Floor & Decor Holdings, Inc. (FND) and Lowe's Companies, Inc. (LOW), has seen its stock rise 6.6% year-to-date. This compares to a 7.3% gain for the overall retail home furnishings industry. Floor & Decor Holdings’ shares have climbed 9%, while Lowe’s has advanced 6.9% over the same period.

From a valuation perspective, Home Depot is trading at a forward price-to-earnings ratio of 24.00, which is above the industry average of 22.08. While Home Depot’s valuation is lower than Floor & Decor Holdings’ forward P/E of 30.75, it is higher than Lowe’s, which stands at 19.98. Home Depot currently holds a Value Score of C.

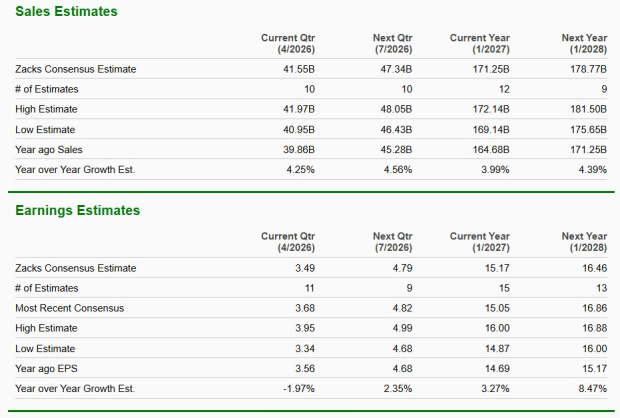

According to Zacks Consensus Estimates, Home Depot’s sales for the current fiscal year are expected to grow by 4% year-over-year, with earnings per share projected to increase by 3.3%. Looking ahead to the next fiscal year, analysts forecast a 4.4% rise in sales and an 8.5% jump in earnings.

Home Depot is currently rated as a Zacks Rank #3 (Hold).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

3 Reasons to Steer Clear of SNX and 1 Alternative Stock Worth Buying

Singapore: Markets weigh Middle East risks – DBS

Hyperliquid and DEXs Break the Top 10 — Is the CEX Era Ending?

Consensus Hong Kong 2026: The Institutional Turn