KeyCorp's Upgrade: Is the Regional Bank Selloff Priced In?

The market's recent mood toward regional banks has been one of sharp unease. That sentiment found a focal point last week when KeyCorpKEY+1.82% shares fell 5.13% to $21.06 in a single session. The catalyst was a weekend blog post that stoked fears of severe economic stress, scenarios Baird later called excessive. The firm's analysis of those fears-projecting 11% unemployment and major credit strain-led it to conclude the resulting selloff was overdone.

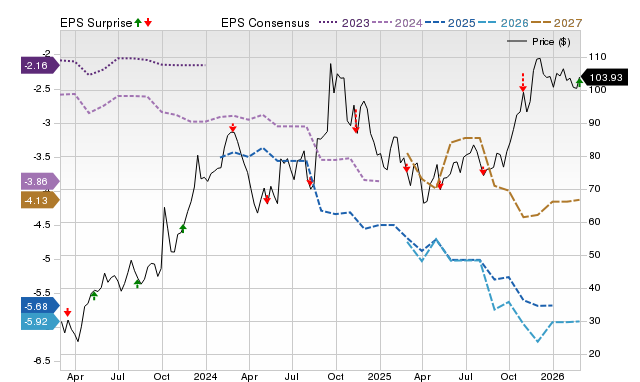

In response, Baird delivered a contrarian move on February 24. The firm upgraded KeyCorp to Neutral from Underperform, explicitly citing the prior day's selloff and the stock's valuation. At a price of about 1.5-times tangible book value, Baird sees a "generally balanced risk/reward trade-off." The upgrade is a clear signal that the firm believes the negative news is already reflected in the share price.

Yet the stock's reaction tells a more nuanced story. Despite the upgrade, shares remain down for the session and are still about 9.8% below its 52-week high. This sets up the central question for investors: has the market's fear been fully priced in, or is the selloff merely a prelude to further weakness? The upgrade suggests the former, but the persistent price decline hints at lingering doubts.

Financial Reality vs. Market Hype

The market's recent selloff, driven by speculative fears, stands in stark contrast to KeyCorp's solid operational performance. The bank's underlying financials tell a story of consistent growth and improving fundamentals, not the stress that has been priced into its stock.

On the top line, KeyCorp delivered a strong quarter. Fourth-quarter revenue exceeded $2.0 billion and grew 12% year-over-year on an adjusted basis. This capped a record year, with full-year revenue reaching $7.5 billion, up 16% year-over-year. More importantly, the quality of that growth was evident. The bank reported that both net interest margin and net interest income came in above the company's earlier targets. Management has now raised its outlook, expecting the net interest margin to climb to roughly 3.00%–3.05% by the end of 2026, a clear signal of operational execution.

Credit metrics also improved. The bank saw nonperforming assets decrease 6% quarter-over-quarter and declines in net charge-offs, criticized loans, and delinquencies. This combination of revenue expansion, margin improvement, and better asset quality paints a picture of a bank executing its strategy effectively.

This operational strength directly contradicts the narrative fueling the selloff. The recent decline in regional bank stocks, including KeyCorp, has been tied to concerns tied to AI and speculative economic fears. Yet those fears have not yet materialized in the bank's financials. The market appears to be pricing in potential future risks-such as a severe economic downturn-that are not reflected in the current quarter's results or the full-year trajectory.

The bottom line is an expectations gap. The bank's fundamentals are improving, with record revenue and better credit quality. The stock, however, is reacting to external sentiment. This creates a setup where the negative news may already be priced in, but the positive operational reality is not yet being fully recognized. For investors, the question is whether the market will eventually reconcile these two realities.

Valuation and the Consensus View

The Baird upgrade hinges on valuation, but the numbers tell a story of a stock that has already moved significantly. KeyCorp trades at roughly 1.5-times tangible book value, a level Baird sees as offering a "generally balanced risk/reward trade-off." This is a key point: the firm believes the stock's price already reflects the recent negative sentiment and selloff. Yet, this valuation is not a discount to intrinsic value in the traditional sense; it's a multiple that has been tested by the market's fear.

The stock's performance over the past year underscores this tension. Shares are up 31.5% over the past year, a strong move that suggests some of the fear has been digested. However, the stock still trades at a discount of about 9% to the average analyst price target. This gap is the core of the investment debate. It indicates that while the market has recovered some ground, a significant portion of the analyst community still sees meaningful upside. The consensus view, with a Hold rating and a $22.92 target price, reflects this cautious optimism.

Analyst sentiment is, in fact, deeply mixed, highlighting the uncertainty. Baird's upgrade to Neutral is a clear shift, but it stands against other views. JPMorgan maintains a Neutral rating with a $24.50 target, while Wells Fargo has an Underperform rating. This divergence shows that even after the selloff, there is no unified conviction on the path forward. The upgrade changes the narrative by arguing the downside is now limited, but it doesn't override the persistent skepticism from other major firms.

The bottom line is that the upgrade likely changes the risk/reward calculus for some investors by removing a negative catalyst. But for the broader market, the setup remains one of priced-in fear with lingering doubts. The stock's rally has been robust, yet the discount to analyst targets and the split in ratings suggest the consensus view is still waiting for clearer signals on economic stress and credit quality. The investment case now depends on whether KeyCorp's improving fundamentals can close that gap.

| 1.09 | 114.48% | Sideways |

| 1.08 | 108.90% | Uptrend |

| 2.28 | 68.89% | Sideways |

| 4.67 | 50.65% | Uptrend |

| 2.34 | 47.17% | Uptrend |

| 1.80 | 46.34% | Sideways |

| 0.46 | 45.77% | Sideways |

| 0.25 | 44.08% | Sideways |

| 84.70 | 35.26% | Uptrend |

| 4.83 | 33.06% | Sideways |

| ALBT Avalon Globocare |

| AEHL Antelope Enterprise |

| RXT Rackspace Technology |

| BFLY Butterfly Network |

| LVWR LiveWire Group |

| MGN Megan Holdings |

| CURX Curanex |

| SAFX XCF Global |

| SEZL Sezzle |

| RRGB Red Robin Gourmet Burgers |

Catalysts and Risks: What to Watch

The investment case for KeyCorp now hinges on a few specific catalysts and risks that will determine if the current valuation holds or if the thesis needs adjustment. The recent selloff and Baird's upgrade have reset the narrative, but the stock's path forward depends on concrete developments and the management's ability to execute its plan.

First, potential acquisition interest from First Citizens BancShares is a major, unresolved variable. Reports indicate the larger bank is weighing a potential acquisition of KeyCorp. If talks progress, this could provide a powerful catalyst for the stock, offering a premium to current levels and validating KeyCorp's strategic value. Until then, the situation remains a speculative overhang that could either support the stock or create uncertainty if the deal falls through. The market will be watching for any formal move from First Citizens.

Second, investors must monitor the execution of management's capital return plan. The bank has signaled strong confidence, with CEO Christopher Gorman stating the company plans to accelerate buybacks, including at least $300 million in the first quarter of 2026. This commitment, coupled with the intentional runoff in low-yield consumer loans, is a key part of the strategy to boost returns. The success of this plan-delivering on buybacks and shifting the balance sheet efficiently-will be a critical test of management's ability to create shareholder value. Any stumble here could undermine the positive operational story.

The primary risk, however, is that speculative fears, even if deemed excessive by analysts, could resurface and pressure the stock. The selloff last week was triggered by a blog post outlining severe economic scenarios, and the market's reaction shows how quickly sentiment can shift. While Baird argues those scenarios are excessive, the stock's volatility and recent decline demonstrate that fear remains a potent force. Broader market sentiment, particularly around banking sector stress or economic data, could reignite these fears and test the stock's resilience at its current, already-pressed levels.

In short, the setup is one of priced-in fear with a potential upside catalyst on the horizon. The stock's ability to hold or rally will depend on whether the First Citizens overhang resolves positively and whether management delivers on its capital return promises. The risk is that external sentiment shifts, reminding the market that even "excessive" fears can be self-fulfilling. For now, the ball is in the court of execution and M&A news.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Earnings Outlook: Algonquin Power & Utilities (AQN) Anticipated Q4 Profit Decrease

Blackbaud and Fortune Brands Innovations have been featured as Zacks Bull and Bear of the Day

MakeMyTrip Q1: Discrepancy Between Growth Projections and Current Valuation

Does Nuvalent (NUVL) Have a Chance to Surge by 37.26% According to Wall Street Analysts?